Building a Fixed Income Portfolio for Retirement in India

07 May 2026 · Sandeep Jain

A practitioner-level guide to building and managing a retirement fixed income portfolio in India, covering corpus sizing, the three-bucket deployment framework, instrument-by-instrument yield data, inflation defence, tax efficiency, and Ultra's specific portfolio recommendations at ₹3 crore, ₹5 crore, and ₹10 crore corpus levels.

Most retirement planning articles in India solve the wrong problem. They tell you how to build a retirement corpus how much to save, what SIP to run, what equity allocation to maintain during the accumulation phase. Very few tell you what to do the day you actually retire: how to convert ₹3, ₹5, or ₹10 crore into a monthly income stream that lasts 25–30 years, keeps pace with inflation, generates enough to cover rising healthcare costs, and does not require daily monitoring.

That is the problem this article solves specifically, from a fixed income perspective.

The investor this article is written for is 55–65 years old, has built a meaningful corpus, and is either approaching or already in retirement. They have ₹25 lakhs minimum in investable surplus, ideally ₹3–10 crore. They want returns above FD rates with manageable risk, are comparing instruments carefully, and cannot afford to make a catastrophic deployment error with money that must last the rest of their life.

The Indian Retirement Reality: Why This Is Harder Than It Looks

India has no meaningful state pension for private sector workers. The EPS (Employees' Pension Scheme) pays a maximum of ₹7,500 per month not enough to cover a month's groceries in a metro. The entire burden of retirement income falls on self-built wealth.

At the same time, Indian retirees face three compounding pressures that make portfolio design more challenging than most articles acknowledge:

Pressure 1: Inflation that is genuinely high. India's long-term CPI inflation averages 6–7% annually. At 6% inflation, ₹1 lakh/month in expenses today becomes ₹1.79 lakhs in 10 years and ₹3.21 lakhs in 20 years. A fixed income portfolio that does not grow its income over time slowly destroys the standard of living it was built to protect.

Pressure 2: Healthcare inflation of 12–14% annually. Medical costs in India are inflating dramatically faster than general prices. A hospitalisation that cost ₹3 lakhs in 2015 costs ₹8–10 lakhs today. A retiree who budgets for healthcare at today's rates and does not build in 12–14% annual cost escalation will face a severe funding gap by their 70s. Most retirement articles acknowledge this in a sentence. This article builds it into the portfolio design.

Pressure 3: Longevity. Indian life expectancy is rising rapidly currently around 70 years average, but a healthy 60-year-old has a meaningful probability of living to 85–90. Planning for a 25-year retirement is a minimum; 30 years is prudent. A corpus that runs out in 20 years is a catastrophic failure, not a near-miss.

The fixed income portfolio must solve all three simultaneously: generate sufficient current income, grow that income over time to offset inflation, and include a specific provision for escalating healthcare costs while never taking risks that could cause a permanent capital loss.

Step 1: Sizing Your Retirement Corpus The Honest Calculation

Before deploying into instruments, confirm your corpus is adequate. The most widely used framework in India is the 25x rule: you need 25 times your annual expenses at retirement as your corpus. This assumes a 4% withdrawal rate a rate at which a well-invested portfolio can sustain withdrawals for 25–30 years.

But the 25x rule significantly underestimates needs for Indian retirees in metro areas. Here is a more precise calculation framework:

| Monthly Expense Today | Monthly Expense at Retirement (6% inflation, 25 years) | Annual Expense at Retirement | Corpus Required (25x) | Corpus Required (30x recommended for metros) | Monthly Income on 10% Yield Corpus |

|---|---|---|---|---|---|

| ₹50,000 | ₹2,15,000 | ₹25.8 Lakhs | ₹6.45 Crore | ₹7.74 Crore | ₹5.38 Lakhs/month |

| ₹75,000 | ₹3,22,000 | ₹38.6 Lakhs | ₹9.66 Crore | ₹11.6 Crore | ₹8.05 Lakhs/month |

| ₹1,00,000 | ₹4,29,000 | ₹51.5 Lakhs | ₹12.9 Crore | ₹15.4 Crore | ₹10.75 Lakhs/month |

The key insight from this table: The 25x rule produces corpus targets that feel large but fixed income instruments in India generating 10% yield can actually service these withdrawals without touching principal at all. A ₹6.45 crore corpus at 10% generates ₹5.38 lakhs/month gross materially more than the ₹2.15 lakhs needed. The excess is reinvested to grow the corpus and offset future inflation.

This is fundamentally different from the 4% withdrawal rate logic developed in the US, where investment-grade bonds yield 4–5%. India's fixed income yield environment allows for a withdrawal strategy that does not require principal drawdown in the early years a critical advantage for longevity planning.

Step 2: The Safe Withdrawal Rate in India's High-Yield Environment

The 4% withdrawal rule was developed by US financial researcher William Bengen in 1994 based on a portfolio of US stocks and bonds. It says: withdraw 4% of your corpus in Year 1, increase the withdrawal by inflation each year, and your corpus should last 30 years.

Applied mechanically to India, this rule is unnecessarily conservative and often confusing, because Indian fixed income yields 8–12% on investment-grade instruments, not 4–5% as in developed markets.

| Portfolio Yield | Safe Annual Withdrawal Rate | Monthly Withdrawal on ₹5 Crore | Portfolio Sustainability | Inflation Buffer |

|---|---|---|---|---|

| 7% (bank FDs and G-Secs only) | 4%–4.5% | ₹1.67–₹1.88 Lakhs | 25–30 years (with 6% inflation eroding capital) | Weak real post-tax return negative at this yield level |

| 9% (FDs + AA corporate bonds) | 5%–5.5% | ₹2.08–₹2.29 Lakhs | 28–35 years | Moderate some corpus growth at lower inflation years |

| 10.5% (Diversified fixed income incl. alternatives) | 6%–7% | ₹2.5–₹2.92 Lakhs | 30–40 years | Strong genuine real return above inflation |

| 12% (Including invoice discounting and private credit) | 7%–8% | ₹2.92–₹3.33 Lakhs | 35–50 years | Very strong portfolio compounds even after withdrawals |

The critical takeaway: A retirement fixed income portfolio generating 10–12% yield in India can support withdrawal rates of 6–8% annually twice the 4% rule while still growing the corpus. This is not a reckless claim. It is the mathematical consequence of India's high fixed income yield environment: if your portfolio earns 12% and you withdraw 8%, your corpus grows 4% annually in nominal terms roughly keeping pace with historical long-term inflation.

This means the retirement fixed income problem in India is fundamentally a yield and instrument selection problem not primarily a savings rate problem. An HNI who retires with ₹5 crore and deploys it at 10–12% in a well-structured fixed income portfolio can sustain ₹25–30 lakhs in annual withdrawals indefinitely.

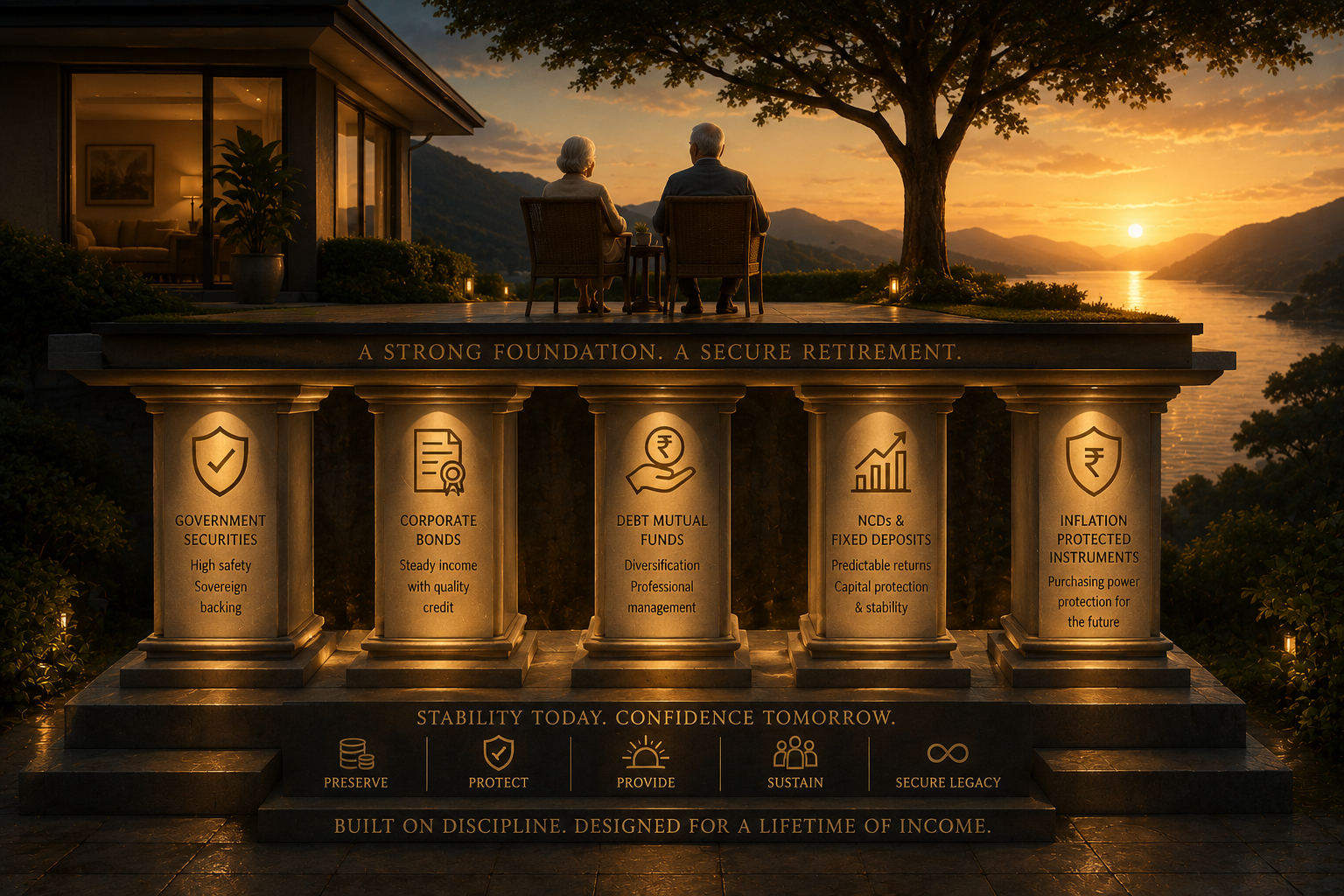

The Three-Bucket Framework for Retirement Fixed Income

The bucket strategy is the most practical framework for structuring a retirement fixed income portfolio. It divides your corpus into three buckets based on time horizon matching the tenure of your investments to the timeline of your cash flow needs.

Why buckets matter: The primary risk in retirement is not poor average returns it is sequence-of-returns risk: the possibility that poor returns in the first 5–7 years of retirement (when withdrawals are largest relative to corpus size) permanently damage the portfolio beyond recovery. The bucket strategy eliminates this risk by ensuring near-term expenses are funded from safe, liquid instruments regardless of what longer-term investments are doing.

Bucket 1: Liquidity and Safety (Years 0–3)

Purpose: Fund the first 3 years of retirement expenses + emergency buffer. Zero risk of capital loss. Fully accessible.

Target allocation: 20–25% of retirement corpus

Instruments:

Bank FDs (scheduled commercial banks): 6.5–7.5% DICGC insured up to ₹5 lakhs per bank. Split across 3–4 banks for full coverage

Senior Citizen Savings Scheme (SCSS): 8.2% government-backed, available to retirees above 60. Maximum ₹30 lakhs per individual (₹60 lakhs joint). Quarterly payouts. Best sovereign rate available to retirees

Post Office Monthly Income Scheme (POMIS): 7.4% government-backed, monthly payouts, ₹9 lakhs limit (single) / ₹15 lakhs (joint)

Liquid mutual funds / Overnight funds: Variable (6.5–7% currently) complete daily liquidity, no exit loads

Monthly income from Bucket 1 (₹1 crore deployed):

SCSS (₹30L at 8.2%): ₹20,500/quarter = ₹6,833/month

POMIS (₹15L at 7.4%): ₹9,250/month

FDs (₹55L at 7%): ₹32,083/month

Total from Bucket 1 (₹1 crore): ~₹48,166/month gross

Bucket 1 generates income while protecting capital absolutely. It is not designed to maximise yield it is designed to ensure you never need to sell a higher-yielding Bucket 2 or 3 instrument at a bad time to pay monthly expenses.

Bucket 2: Income Engine (Years 3–15)

Purpose: Generate the bulk of retirement income higher yield, longer tenure, moderate liquidity. The primary inflation-fighting engine.

Target allocation: 55–60% of retirement corpus

Instruments:

AA corporate bonds / NCDs (monthly payout): 9.5–10.5% the workhorse of retirement fixed income. Monthly coupon payments, predictable, SEBI-regulated. Ladder maturities across 1, 2, 3, and 5 years

Tax-free PSU bonds (NHAI, PFC, IRFC secondary market): 7.64–8.75% tax-free coupon for investors in the 30%+ bracket, equivalent to 11–13% taxable. No TDS, no annual tax filing complexity

Invoice discounting (strong corporate / PSU buyers): 10–15% annualised the most powerful yield generator in Bucket 2. 30–90 day tenure means rapid capital recycling

Asset leasing: 10–14% with monthly payouts tangible asset backing, monthly income, 2–4 year tenures

RBI Floating Rate Savings Bond: 8.05% sovereign quality, automatic rate adjustment if rates rise. 7-year tenure. Semi-annual payouts

Why invoice discounting belongs in retirement portfolios: This requires addressing directly, because most retirement planning advice completely ignores it. Invoice discounting on PSU and large corporate buyers at 11–13% delivers more monthly income per rupee than any other investment-grade instrument available. The 30–90 day tenure means your capital returns continuously providing the liquidity of Bucket 1 at the yield of Bucket 2.

For a ₹50 lakh allocation in invoice discounting at 12%, a retiree generates approximately ₹50,000/month gross (₹35,000 post-30% tax). That is ₹35,000 in real monthly income from ₹50 lakhs compared to ₹24,500/month gross (₹17,150 post-tax) from the same corpus in a bank FD. The difference of ₹17,850/month is ₹2.14 lakhs annually money that either funds expenses directly or reinvests to grow the corpus.

For detailed guidance on invoice discounting as an investment, read: Invoice Discounting as an Investment

Monthly income from Bucket 2 (₹2.5 crore deployed, illustrative mix)

| Instrument | Allocation | Yield | Gross Monthly Income | Post-Tax Monthly (30%) |

|---|---|---|---|---|

| AA Corporate NCDs (monthly coupon) | ₹75 Lakhs | 10% | ₹62,500 | ₹43,750 |

| Tax-Free PSU Bonds | ₹50 Lakhs | 8% (tax-free) | ₹33,333 | ₹33,333 (no tax) |

| Invoice Discounting (large corporates) | ₹75 Lakhs | 12% | ₹75,000 | ₹52,500 |

| Asset Leasing | ₹25 Lakhs | 11% | ₹22,917 | ₹16,042 |

| RBI Floating Rate Bond | ₹25 Lakhs | 8.05% | ₹16,771 | ₹11,740 |

| TOTAL | ₹2.5 Crore | ~10.2% blended | ₹2,10,521 | ₹1,57,365 |

₹1.57 lakhs per month post-tax from ₹2.5 crore in Bucket 2. That is a real, sustainable monthly income stream not a theoretical projection. At a 6% withdrawal rate on ₹2.5 crore, you need ₹1.25 lakhs/month to maintain corpus. This deployment generates ₹32,365 more per month the surplus either funds expenses or compounds the corpus.

Bucket 3: Inflation Defence and Legacy (Years 15+)

Purpose: Long-horizon growth that keeps the overall portfolio's real purchasing power intact across 25–30 years of retirement. Less focus on current income, more on capital appreciation and inflation protection.

Target allocation: 20–25% of retirement corpus

Instruments:

Equity (direct or through PMS/MF SWP): 15–20% of total corpus the only proven long-term inflation beater. For a 60-year-old, a 20–25% equity allocation is appropriate and necessary to prevent the fixed income portfolio from being slowly destroyed by inflation

Sovereign Gold Bonds (existing holdings NRIs cannot buy new): 2.5% coupon + gold price inflation hedge. Full CGT exemption at 8-year maturity

REITs (Embassy, Mindspace, Brookfield): 7–9% distribution yield + rental escalation. Commercial real estate income that grows with CPI

Long-duration G-Secs (10–30 year): 6.7–7% in a falling rate environment, price appreciation adds to total return. Capital protection with upside if rate cycle continues lower

Why Bucket 3 must exist even in a "fixed income" retirement portfolio: This is the most counterintuitive but most important point in this article. A 60-year-old retiree who puts 100% of their corpus in fixed income even at 10–12% yield will see their purchasing power erode over a 25-year retirement. At 6% inflation, prices double every 12 years. The corpus must have components that grow in real terms.

Bucket 3 is not speculation it is structured, long-horizon inflation insurance. The 20–25% allocation is sized so that even in a prolonged equity downturn, Bucket 1 and Bucket 2 fully fund expenses for 15+ years without requiring any sale from Bucket 3.

Fixed Income Instrument Selection: What to Use and Why

| Instrument | Yield | Post-Tax Yield (30%) | Payout | Tenure | Role in Retirement Portfolio | Key Risk |

|---|---|---|---|---|---|---|

| Senior Citizen Savings Scheme (SCSS) | 8.2% | 5.74% | Quarterly | 5 years (extendable) | Bucket 1 sovereign foundation | TDS on interest; reinvestment risk at maturity |

| Post Office MIS (POMIS) | 7.4% | 5.18% | Monthly | 5 years | Bucket 1 monthly income base | Cap of ₹15L joint; reinvestment risk |

| Bank FD | 6.5%–7.9% | 4.55%–5.53% | Monthly / Quarterly / At maturity | 7 days–10 years | Bucket 1 liquidity buffer | DICGC only covers ₹5L; reinvestment risk |

| Tax-Free PSU Bonds (secondary) | 7.64%–8.75% (tax-free) | 7.64%–8.75% (no tax) | Annual / Semi-annual | Remaining to maturity | Bucket 2 tax-efficient income core | Thin secondary market; price risk if sold early |

| AA Corporate NCD (monthly) | 9.5%–10.5% | 6.65%–7.35% | Monthly | 1–5 years | Bucket 2 income engine core | Issuer credit risk; reinvest at lower rates at maturity |

| Invoice Discounting (PSU/large corporate) | 10%–15% | 7%–10.5% | Bullet at maturity (30–90 days) | 30–90 days | Bucket 2 highest yield, rapid recycling | Buyer payment delay; no secondary market |

| Asset Leasing | 10%–14% | 7%–9.8% | Monthly | 2–4 years | Bucket 2 stable monthly income with asset backing | Lessee default; asset depreciation |

| RBI Floating Rate Savings Bond | 8.05% (resets every 6M) | 5.64% | Semi-annual | 7 years | Bucket 2 inflation hedge if rates rise | Lock-in; coupon falls if rates cut further |

| REITs (Embassy, Mindspace) | 7%–9% distribution | 6.5%–8% blended (partial tax-free) | Quarterly | Listed open ended | Bucket 3 inflation-linked income with real asset growth | Commercial real estate cycle; listed price volatility |

For a complete guide to corporate bonds and their return profiles, read: Best Corporate Bonds in India 2026. For the full monthly income bonds guide, read: Monthly Income from Bonds in India: How It Works.

The Healthcare Inflation Problem: Building a Medical Buffer

Most retirement fixed income articles mention healthcare costs in a paragraph. This one builds it into the portfolio.

Healthcare inflation in India runs at 12–14% annually roughly double general CPI inflation. A hospitalisation that costs ₹5 lakhs today will cost ₹18–22 lakhs in 10 years. Surgical procedures, long-term care, specialist consultations, and chronic disease management compound relentlessly.

The practical solution is two-part:

Health insurance: A ₹1 crore super top-up health insurance policy combined with a base floater of ₹5–10 lakhs covers most hospitalisation events at a reasonable annual premium of ₹60,000–₹1.2 lakhs. This is the first line of defence and should be established before retirement, while you are still insurable.

Healthcare corpus within the portfolio: Set aside a dedicated sub-corpus of ₹25–50 lakhs specifically for healthcare deployed in Bucket 1 instruments (SCSS, FDs) and ring-fenced from regular expense withdrawals. This is replenished by income generated from Bucket 2. The discipline of ring-fencing prevents healthcare emergencies from forcing premature liquidation of Bucket 2 or Bucket 3 investments at unfavourable times.

Monthly healthcare budget: Build explicit healthcare expense escalation into your withdrawal planning assume healthcare costs grow at 10% per year (conservative relative to actual 12–14%) and ensure your withdrawal rate targets the healthcare-inclusive expense figure, not just lifestyle expenses.

Tax Optimisation for Retirement Fixed Income

Tax efficiency in retirement is not optional it is the difference between a portfolio that sustains itself and one that slowly depletes. For retirees in the 30% bracket:

Strategy 1 Maximise tax-free instruments first: Tax-free PSU bonds (coupon fully exempt), POMIS (interest taxable but Senior Citizen threshold applies), and SCSS (taxable but 80TTB deduction available) should all be deployed before taxable corporate bonds. The 80TTB deduction allows senior citizens (above 60) to deduct up to ₹50,000 annually in interest income from banks, FDs, and post office instruments a ₹15,000 annual tax saving that should be maximised.

Strategy 2 Use the PPF legacy corpus tax-free: If you built a PPF corpus during working years, it is EEE (Exempt-Exempt-Exempt) withdrawals are completely tax-free. PPF corpus in retirement provides a tax-free income stream that reduces the effective tax rate on your blended portfolio income.

Strategy 3 Spread taxable income across family members: If your spouse has a lower income or no income, routing a portion of fixed income investments through joint accounts or in their name can reduce the blended household tax rate. Interest income is taxed in the hands of the earning member structure investments accordingly with a CA's guidance.

Strategy 4 LTCG arbitrage on bond sale: If you buy listed bonds in the secondary market and sell them after 12 months at a profit (in a falling rate environment where bond prices rise), the capital gain is taxed at 12.5% versus 30% on coupon income. For sophisticated retirees, this creates opportunities to generate income through price appreciation at a lower effective tax rate.

For a comprehensive guide on tax-saving strategies, read: Tax-Saving Investment Options for HNIs in India FY 2025–26.

Real Portfolios: Deployment Frameworks at ₹3 Crore, ₹5 Crore, and ₹10 Crore

| Allocation | ₹3 Crore Corpus | ₹5 Crore Corpus | ₹10 Crore Corpus |

|---|---|---|---|

| Bucket 1 Safety & Liquidity (20–25%) | ₹65L SCSS ₹30L, POMIS ₹15L, FDs ₹20L | ₹1Cr SCSS ₹30L, POMIS ₹15L, FDs ₹55L | ₹2Cr SCSS ₹60L, POMIS ₹30L, FDs ₹1.1Cr |

| Bucket 2 Income Engine (55–60%) | ₹1.7Cr AA NCDs ₹50L, Tax-Free Bonds ₹40L, Invoice Discounting ₹50L, Asset Leasing ₹30L | ₹3Cr AA NCDs ₹75L, Tax-Free Bonds ₹50L, Invoice Discounting ₹1Cr, Asset Leasing ₹75L | ₹5.5Cr AA NCDs ₹1Cr, Tax-Free Bonds ₹1.5Cr, Invoice Discounting ₹2Cr, Asset Leasing ₹1Cr |

| Bucket 3 Inflation Defence (20–25%) | ₹65L Equity MF/PMS ₹50L, REITs ₹15L | ₹1Cr Equity MF/PMS ₹75L, REITs ₹25L | ₹2.5Cr Equity PMS ₹1.5Cr, REITs ₹50L, Long G-Secs ₹50L |

| Healthcare buffer (ring-fenced within Bucket 1) | ₹25L in separate FD | ₹35L in separate FD | ₹50L in liquid fund |

| Blended portfolio yield (Buckets 1+2) | ~9.5% | ~10% | ~10.5% |

| Estimated gross monthly income (Buckets 1+2) | ~₹1.82 Lakhs | ~₹3.33 Lakhs | ~₹6.87 Lakhs |

| Estimated post-tax monthly income (30% bracket) | ~₹1.27 Lakhs | ~₹2.33 Lakhs | ~₹4.81 Lakhs |

What these portfolios are designed to do

Generate sufficient post-tax monthly income for the stated corpus size

Bucket 1 funds the first 3 years of expenses while Bucket 2 compounds

Invoice discounting in Bucket 2 provides the highest yield component with 30–90 day recycling

Tax-free bonds maximise post-tax income for investors in 30%+ brackets

Bucket 3 equity/REIT allocation grows the overall corpus against inflation over 15–20 years

For a broader view of high-yield fixed income options, read: Best Fixed Income Investments in India 2026.

FAQs

Q1. How much corpus do I need to retire in India in 2026?

A practical rule: 25–30 times your annual expenses at retirement (25x if you have other income sources; 30x if your corpus is your only income). For a retiree needing ₹1.5 lakhs/month (₹18 lakhs/year) at retirement, the required corpus is ₹4.5–5.4 crore. In India's high-yield fixed income environment, a ₹5 crore corpus invested at 10% can generate ₹4.17 lakhs/month gross substantially more than the withdrawal rate requires, providing a real inflation buffer.

Q2. Is it safe to invest in corporate bonds in retirement?

Yes at the AA and AAA rating level. Diversified across 8–10 issuers from different sectors, AA-rated corporate bonds have historically had very low default rates in India. The key is diversification: never put more than 10–15% of your bond portfolio in a single issuer, stick to AA and above ratings, and prefer secured NCDs over unsecured bonds.

Q3. Should I put all my retirement corpus in fixed income?

No. A pure fixed income portfolio, even at 10–12% yield, cannot maintain purchasing power over a 25–30 year retirement at 6% annual inflation. A 20–25% allocation to growth instruments (equity mutual funds, PMS, or REITs) is necessary to ensure the portfolio's real value grows over time. The three-bucket strategy addresses this explicitly Bucket 3 provides the inflation protection that pure fixed income cannot.

Q4. What is the safest monthly income option for Indian retirees?

The Senior Citizen Savings Scheme (SCSS) at 8.2% quarterly and Post Office Monthly Income Scheme (POMIS) at 7.4% monthly are the safest options both government-backed. Together, they can provide approximately ₹2.5–3 lakhs/month for a couple maximising both schemes. For additional safety + yield, AA-rated monthly-payout corporate NCDs add income with manageable credit risk. For maximum yield at manageable risk, invoice discounting on PSU buyers adds a significant layer without materially increasing portfolio risk.

Q5. How should healthcare costs be factored into a retirement fixed income portfolio?

Healthcare inflation in India runs at 12–14% annually significantly above general CPI. The practical approach is two-part: maintain a comprehensive health insurance policy (₹1 crore super top-up) to cover large hospitalisation events, and ring-fence a dedicated healthcare corpus of ₹25–50 lakhs within Bucket 1 that is never drawn for regular expenses. This prevents healthcare emergencies from forcing premature liquidation of Bucket 2 positions.

Q6. Is invoice discounting suitable for retirement portfolios?

Yes for investors who understand the instrument and maintain proper diversification. Invoice discounting on large corporate and PSU buyers delivers 10–15% yields on 30–90 day tenures. The credit risk is on the buyer (a large corporate or PSU), not the MSME seller. With diversification across 15–20 invoices from different buyers, a ₹50 lakh invoice discounting allocation can generate ₹50,000/month gross at 12% yield approximately double the equivalent bank FD income. It belongs in Bucket 2 of a retirement portfolio, not as a speculative add-on.

Disclaimer

This article is for informational and educational purposes only and does not constitute investment or financial planning advice. Returns mentioned are indicative based on current market conditions in 2026. All investments carry risk. Retirement planning involves individual-specific factors that this article cannot address. Please consult a SEBI-registered investment advisor and a certified financial planner before making retirement portfolio decisions.