Best Fixed Income Investments in India 2026: Ranked by Risk and Return

08 April 2026 · Sachin Gadekar

A comprehensive, honest comparison of every major fixed income investment option in India — ranked from lowest to highest risk, with real return figures, so you can build the right portfolio for your goals.

What Is Fixed Income Investing?

Fixed income investing in India has never been more varied — or more confusing. On one end, you have sovereign-backed government instruments yielding 7–8%. On the other, alternative fixed income options delivering 12–15%. In between, there are corporate bonds, NCDs, debt mutual funds, and a dozen other instruments, each with different risk profiles, tenures, tax treatments, and return characteristics.

Most articles on this topic cover either the safe end (PPF, FDs, G-Secs) or the high-yield end (invoice discounting, alternative investments) — but rarely both together in a single honest comparison.

This guide covers the complete fixed income spectrum — 10 investment types ranked from lowest to highest risk — so you can build a portfolio that matches your goals, not just your comfort zone.

Fixed income investing refers to deploying capital into instruments that pay a predetermined, regular return — unlike equity where returns depend on company performance and market sentiment. The "fixed" refers to the predictability of cash flows, not necessarily that the rate never changes.

Fixed income serves three core functions in a portfolio:

Capital preservation protecting your principal from erosion

Regular income generating predictable cash flows for expenses or reinvestment

Portfolio stability balancing volatility from equity holdings

In India, fixed income options range from near-zero risk sovereign instruments to higher-yielding alternative instruments with very different risk-return trade-offs across the spectrum.

How to Read This Guide

We rank all 10 instruments from lowest to highest risk. For each option, we cover:

Typical returns in 2026

Who it is best suited for

Key risks

Liquidity and tenure

Tax treatment

The goal is not to declare one instrument the best, it is to help you understand which combination is right for your situation.

1. Government Securities (G-Secs and T-Bills)

Return: 6.8%–7.5% | Risk: Lowest possible

Government Securities (G-Secs) are bonds issued by the Government of India to fund its borrowing needs. They carry a sovereign guarantee, the closest thing to a risk-free investment in India. T-Bills are short-term versions (91, 182, or 364 days); dated G-Secs run up to 40 years.

Retail investors can now buy G-Secs directly through the RBI Retail Direct platform, commission-free, with no minimum beyond ₹10,000.

Best for: Ultra-conservative investors, retirees seeking capital safety, and those wanting to park money in 100% sovereign instruments.

Key limitation: Returns barely keep pace with inflation. At 7–7.5%, a 30% tax bracket investor earns only ~5% post-tax, which is below the long-term inflation average.

Liquidity: High, listed on exchanges and tradeable in the secondary market.

2. RBI Floating Rate Savings Bonds

Return: 8.05% (resets every 6 months) | Risk: Sovereign

These bonds are issued by the Reserve Bank of India and carry a full sovereign guarantee. The interest rate is linked to the National Savings Certificate (NSC) rate plus a 0.35% spread currently at 8.05% p.a., paid semi-annually.

The floating rate feature means returns adjust with the broader interest rate environment making them a better inflation hedge than fixed G-Secs.

Best for: Investors seeking guaranteed income above FD rates for a 7-year period without any credit risk.

Key limitation: 7-year lock-in with no premature redemption (except for senior citizens with age-based concessions). Fully taxable as per income slab.

Liquidity: Low not tradeable in secondary market.

3. PPF and Small Savings Schemes

| Scheme | Return | Tenure | Tax Benefit | Best For |

|---|---|---|---|---|

| PPF | 7.1% | 15 years | EEE (fully tax-free) | Long-term, tax-free wealth building |

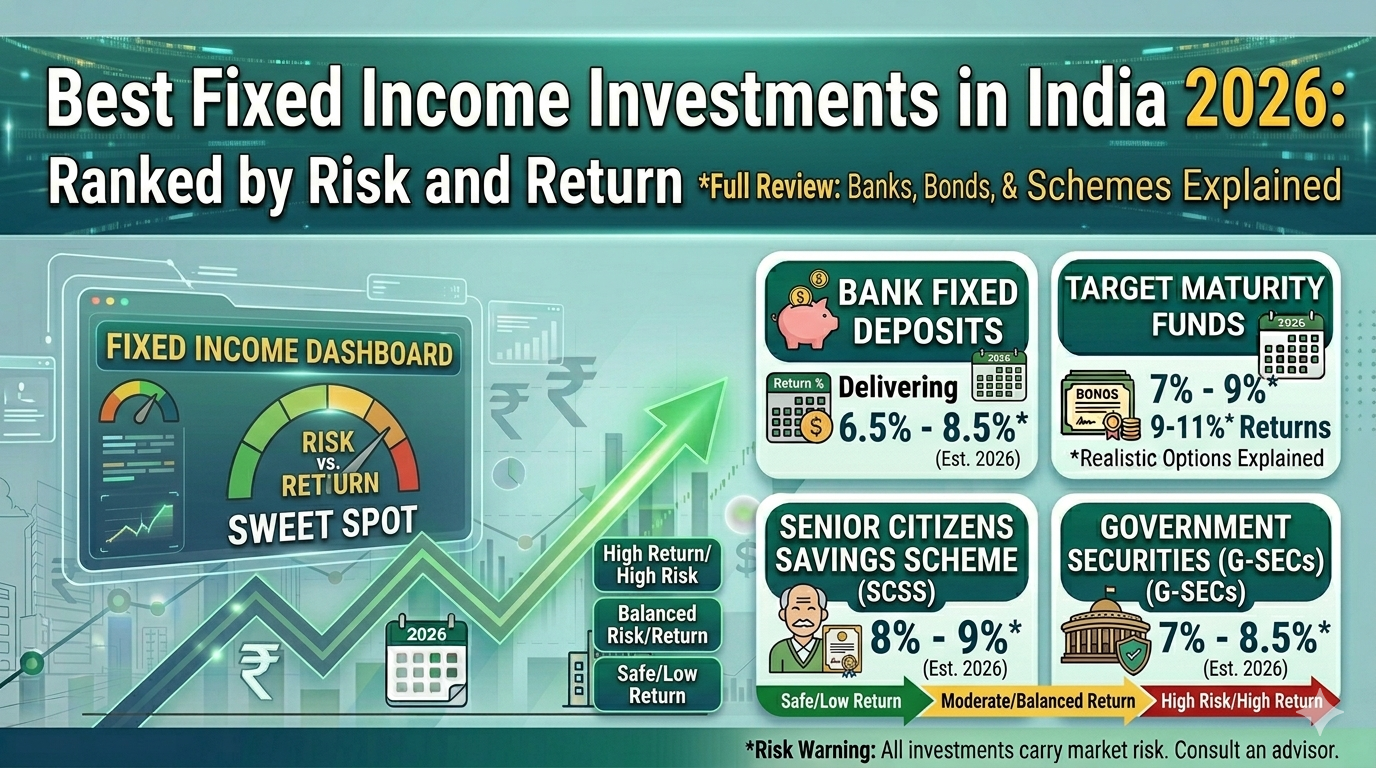

| SCSS | 8.2% | 5 years | 80C deduction; income taxable | Senior citizens seeking quarterly income |

| NSC | 7.7% | 5 years | 80C deduction; interest taxable | Conservative mid-term investors |

| POMIS | 7.4% | 5 years | None | Monthly income seekers (up to ₹9L single/₹15L joint) |

4. Bank Fixed Deposits

Return: 6.5%–7.5% (up to 8.5% for senior citizens) | Risk: Very Low

Bank FDs remain the most widely used fixed income instrument in India. Deposits up to ₹5 lakhs are insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC) making them effectively risk-free at that level.

Small finance banks and some scheduled banks offer up to 8–9% meaningfully higher than large PSU or private banks but with marginally higher institutional risk.

Best for: Emergency fund parking, conservative investors who prioritise capital safety, and investors with investment horizons of 1–5 years.

Key limitation: Returns are fully taxable. TDS is deducted at source on interest above ₹40,000/year (₹50,000 for senior citizens). At the 30% bracket, a 7.5% FD yields only ~5.25% post-tax.

Liquidity: Good most banks allow premature withdrawal with a penalty of 0.5–1%.

5. Corporate Fixed Deposits

Return: 8%–9.5% | Risk: Low–Moderate

Corporate FDs are fixed deposits offered by Non-Banking Financial Companies (NBFCs) and manufacturing companies not banks. They are not covered by DICGC insurance, which is why they offer higher rates to compensate for the slightly elevated risk.

Well-known corporate FD issuers include Bajaj Finance, Mahindra Finance, Shriram Finance, and HDFC Ltd. AAA-rated corporate FDs from these companies are considered highly reliable.

Best for: Investors seeking meaningfully better returns than bank FDs without entering the bond market.

Key limitation: Not DICGC insured. Credit risk depends entirely on the issuing company. Returns are fully taxable.

Liquidity: Generally available with premature withdrawal (with penalty), but not as liquid as bank FDs.

6. Debt Mutual Funds

Return: 6.5%–8.5% (varies by category) | Risk: Low–Moderate

Debt mutual funds invest in a diversified portfolio of fixed income instruments G-Secs, corporate bonds, T-Bills, and commercial papers. They are professionally managed, SEBI-regulated, and offer excellent liquidity for most categories.

Key categories and typical returns:

Liquid funds: 6.5–7% (overnight to 91-day instruments)

Short-term debt funds: 7–8%

Corporate bond funds: 7.5–8.5%

Credit risk funds: 8–10% (higher credit risk)

Best for: Investors who want fixed income diversification without selecting individual bonds, with the added benefit of professional management and daily liquidity for most fund types.

Key limitation: Returns are not guaranteed — they vary with interest rate movements and credit events. Unlike individual bonds, you cannot lock in a specific yield. All income is now taxed at slab rate (post the 2023 budget change).

7. AAA-Rated Corporate Bonds and NCDs

Return: 8%–9.5% | Risk: Moderate (well-managed)

Listed Non-Convertible Debentures (NCDs) and bonds issued by AAA-rated companies — Tata Capital, Bajaj Finance, HDFC Bank, REC, PFC — offer fixed coupon payments over defined tenures, with returns typically 100–200 basis points above comparable G-Secs.

These are SEBI-regulated, exchange-listed instruments that can be bought through your demat account or via platforms like Jiraaf, Wint Wealth, GoldenPi, and Ultra.

Best for: Investors who want better returns than bank FDs and corporate FDs, with the added benefit of secondary market liquidity. Ideal for those building a fixed income ladder with known cash flows.

Key limitation: Secondary market liquidity can be thin for smaller bond lots. Interest income is taxable at slab rate.

Liquidity: Moderate — listed on BSE/NSE, but actual secondary market depth varies by issuance size.

8. High-Yield Corporate Bonds (AA and Below)

Return: 10%–13% | Risk: Moderate–High

Moving down the credit rating spectrum from AAA to AA, A, or BBB opens up meaningfully higher yields. NBFCs, mid-sized real estate companies, and infrastructure firms regularly issue bonds and NCDs in this range at 10–13%.

This is where the risk-return trade-off becomes more meaningful. A lower rating does not mean imminent default AA is still investment grade but it does mean higher probability of financial stress compared to AAA issuers.

Best for: Investors with a higher risk tolerance who understand credit risk and are willing to accept yield for it. Ideal for the "satellite" portion of a fixed income portfolio.

Key limitation: Thorough credit due diligence is essential. Avoid chasing yield without examining issuer financials, debt levels, and sector exposure.

9. Invoice Discounting

Return: 10%–15% | Risk: Moderate

Invoice discounting sits in the alternative fixed income space — but is one of the most transparent and accessible options within it. Businesses sell their invoices to investors at a discount; investors earn the margin when the invoice is paid by the corporate buyer.

The key differentiator from bonds: tenures are very short (30–90 days), returns are pre-agreed before investment, and the risk is primarily the creditworthiness of the invoice payer — often a large, listed corporate.

Best for: Investors wanting 10%+ returns with short tenures and rapid capital recycling. Excellent for building passive income through frequent reinvestment cycles.

Key limitation: Capital is locked until invoice maturity — no early exit. Diversification across multiple invoices is essential to manage payer default risk.

Platforms: ultra, altGraaf, KredX, TradeCred.

10. Asset Leasing and Securitised Debt Instruments

Return: 10%–14% | Risk: Moderate

Asset leasing involves co-investing in physical assets — trucks, medical equipment, machinery — and earning lease rental income. Securitised Debt Instruments (SDIs) pool multiple receivables into a structured product that investors buy as a single unit.

Both offer 10–14% returns with non-market-correlated income, and both are structured to provide regular payouts (typically monthly).

Best for: Investors wanting asset-backed passive income or diversified debt exposure in a single structured product. Particularly popular with HNIs building alternative fixed income portfolios.

Key limitation: Less liquid than bonds — exit before tenure is usually not possible. Minimum diligence required on underlying asset quality or receivables pool.

Platforms: ultra.

Master Comparison Table: All 10 Options Ranked

| Rank (Low to High Risk) | Instrument | Typical Return (2026) | Tenure | Min. Investment | Liquidity | Tax Treatment | Best For |

|---|---|---|---|---|---|---|---|

| 1 | G-Secs / T-Bills | 6.8%–7.5% | 91 days to 40 years | ₹10,000 | High | Slab rate | Capital safety, sovereign guarantee |

| 2 | RBI Floating Rate Bonds | 8.05% | 7 years | ₹1,000 | Very Low | Slab rate | Inflation-linked sovereign income |

| 3 | PPF / SCSS / NSC / POMIS | 7.1%–8.2% | 5–15 years | ₹500–₹1,000 | Low | PPF: Tax-free; others: Slab rate | Tax-efficient long-term savings |

| 4 | Bank FDs | 6.5%–7.5% | 7 days to 10 years | ₹1,000 | High (with penalty) | Slab rate + TDS | Conservative parking, capital safety |

| 5 | Corporate FDs | 8%–9.5% | 1–5 years | ₹5,000–₹25,000 | Moderate | Slab rate + TDS | Better FD returns, known issuers |

| 6 | Debt Mutual Funds | 6.5%–8.5% | Flexible | ₹500+ | High (T+1 to T+3) | Slab rate | Liquidity + diversification |

| 7 | AAA Corporate Bonds / NCDs | 8%–9.5% | 1–10 years | ₹10,000–₹1L | Moderate | Slab rate | Better yield vs FD, secondary liquidity |

| 8 | High-Yield Bonds / NCDs (AA and below) | 10%–13% | 1–5 years | ₹10,000–₹1L | Moderate | Slab rate | Yield seekers comfortable with credit risk |

| 9 | Invoice Discounting | 10%–15% | 30–90 days | ₹25,000–₹1L | Low (locked till maturity) | Slab rate | Short-term high yield, HNIs |

| 10 | Asset Leasing / SDIs | 10%–14% | 6 months–4 years | ₹10,000–₹1L | Low | Slab rate | Asset-backed passive income, HNIs |

How to Choose the Right Fixed Income Mix

No single instrument on this list is universally "best." The right mix depends on three variables:

1. Your return requirement If you need 7–8% with zero risk tolerance stick to G-Secs, RBI Bonds, and bank FDs. If you want 10–12% and can accept moderate credit risk, move into high-yield bonds and invoice discounting.

2. Your liquidity needs If you may need funds within 3–6 months priorities debt mutual funds and bank FDs with premature withdrawal options. If your capital is patient allocate more to asset leasing and invoice discounting for the higher yields.

3. Your tax situation At the 30% bracket, a 9% gross return becomes ~6.3% post-tax. This makes higher-yield instruments even more attractive in absolute post-tax terms, as long as the credit risk is manageable. PPF remains the gold standard for tax-free compounding despite the 7.1% rate.

Fixed Income Portfolio Examples by Investor Type

| Investor Type | Conservative Allocation | Moderate Allocation | Aggressive Allocation | Expected Blended Return |

|---|---|---|---|---|

| Retiree / Senior Citizen | 40% SCSS + 30% RBI Bonds + 20% Bank FD + 10% AAA Bonds | 30% SCSS + 20% RBI Bonds + 25% AAA Bonds + 25% Invoice Discounting | 20% SCSS + 20% AAA Bonds + 30% High-Yield Bonds + 30% Invoice Discounting | 7.5% / 9.5% / 11.5% |

| Working Professional (30–45) | 40% PPF + 30% Bank FD + 30% Debt MF | 20% PPF + 20% Bank FD + 30% AAA Bonds + 30% Invoice Discounting | 10% PPF + 20% High-Yield Bonds + 40% Invoice Discounting + 30% Asset Leasing | 7% / 9.5% / 11.5% |

| HNI (₹50L+ corpus) | 30% G-Secs + 30% AAA Bonds + 40% Corporate FD | 20% AAA Bonds + 30% High-Yield Bonds + 30% Invoice Discounting + 20% Asset Leasing | 10% AAA Bonds + 30% High-Yield Bonds + 40% Invoice Discounting + 20% SDIs | 8% / 10.5% / 12% |

Q1. What is the best fixed income investment in India for 2026?

There is no single best option — it depends on your risk tolerance, tenure, and tax bracket. For guaranteed safety, G-Secs and RBI Bonds are unmatched. For 10%+ returns with moderate risk, invoice discounting and high-yield NCDs are the strongest options.

Q2. Which fixed income investment gives the highest return in India?

Invoice discounting (10–15%) and asset leasing (10–14%) deliver the highest predictable returns. P2P lending can go higher (12–18%) but carries more risk. All come with credit risk and limited liquidity.

Q3. Is PPF still worth it in 2026?

Yes, but only for its tax benefit, not its return. PPF's 7.1% rate is not impressive, but its EEE (Exempt-Exempt-Exempt) status makes it irreplaceable for high-bracket investors building a tax-free long-term corpus. The 15-year lock-in is the main trade-off.

Q4. How should I split between safe and higher-yield fixed income?

A common framework: 50–60% in safer instruments (G-Secs, bank FDs, AAA bonds) and 30–40% in higher-yield alternatives (invoice discounting, high-yield bonds, asset leasing). Adjust based on your income needs and risk comfort.

Q5. Are corporate bonds safer than bank FDs?

Not necessarily. Bank FDs are DICGC-insured up to ₹5 lakhs — making them effectively risk-free at that level. AAA-rated corporate bonds are very safe but not insured. High-yield bonds carry more credit risk than bank FDs. The higher yield is compensation for that difference.

Q6. How is fixed income taxed in India?

Most fixed income returns — FD interest, bond coupons, invoice discounting income — are taxed as interest income under your applicable slab rate. PPF is the only mainstream fixed income instrument with fully tax-free returns. Tax-free bonds (NHAI, PFC) also offer tax-free coupon income but are rarely issued now.

Disclaimer

This article is for informational purposes only and does not constitute investment advice. Returns are indicative and based on current market conditions. All investments carry risk. Please consult a registered financial advisor before investing.