TReDS in India: What It Is and How Investors Can Benefit (2026)

18 June 2026 · Sachin Gadekar

A complete explainer of India's Trade Receivables Discounting System (TReDS) how RXIL, M1xchange, and Invoice Mart work, the Union Budget 2026-27 CPSE mandate that is reshaping the MSME financing landscape, and how investors can benefit from the structural growth of this market.

If you have read anything about invoice discounting in India recently including the articles on this site you have likely encountered the acronym TReDS. The Union Budget 2026-27's mandate requiring Central Public Sector Enterprises (CPSEs) to use TReDS has been described as one of the most significant structural tailwinds for invoice discounting in years. But what exactly is TReDS, how does it actually work, and what does its growth mean for investors?

This article explains TReDS from the ground up the three RBI-licensed platforms, how the auction mechanism works, the scale of the market and its 2026 growth trajectory, and crucially, how the TReDS ecosystem relates to (and differs from) the invoice discounting opportunities available to individual investors.

What Is TReDS? The Plain English Explanation

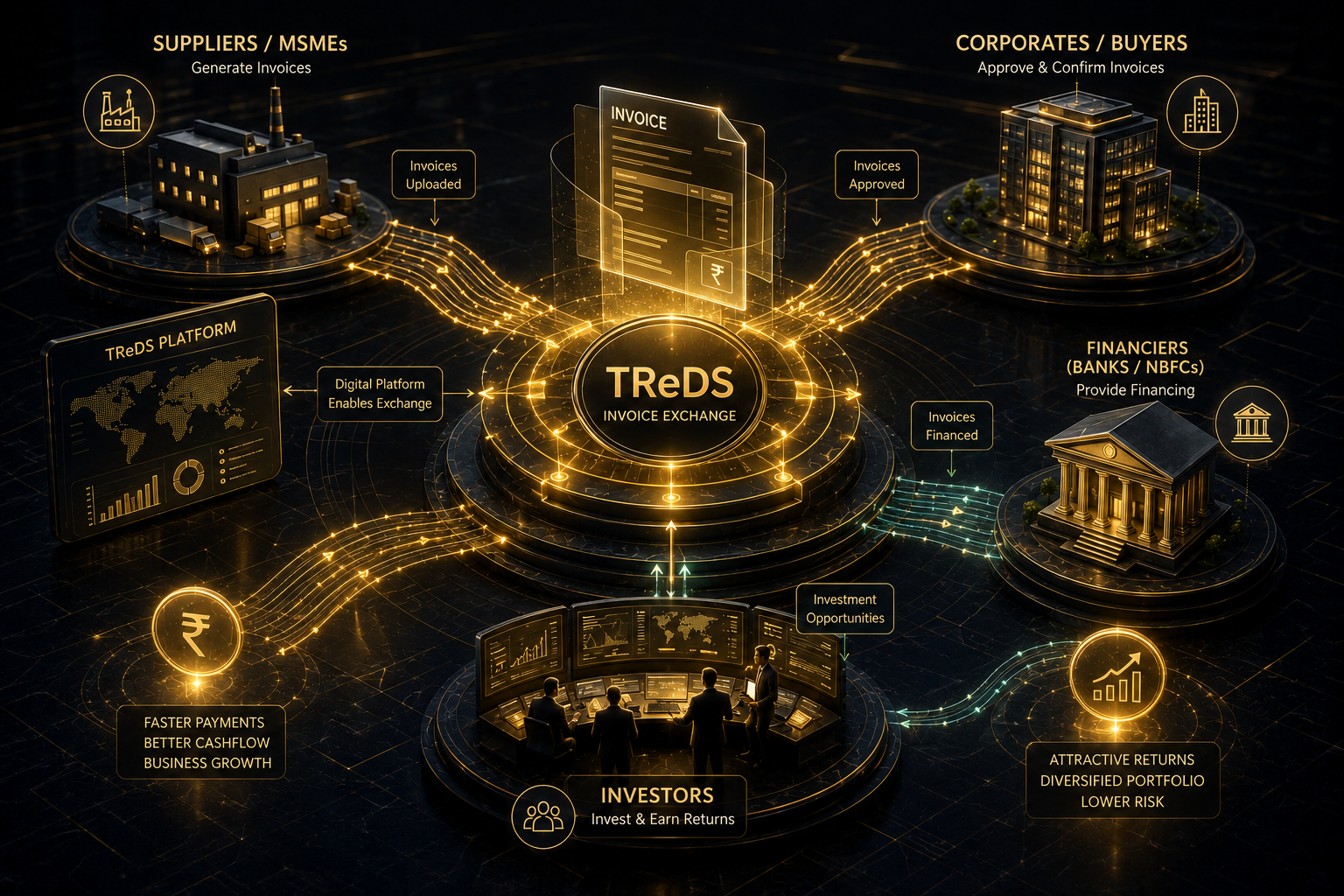

TReDS stands for Trade Receivables Discounting System an RBI-regulated electronic platform that allows MSMEs (Micro, Small, and Medium Enterprises) to convert their unpaid invoices from large corporate buyers into immediate cash, by auctioning those invoices to a competing pool of banks and NBFCs.

In plain terms: an MSME supplies goods or services to a large corporate buyer. The buyer's payment terms are typically 30, 45, or 60 days. Rather than wait for that payment, the MSME uploads the invoice (approved by the buyer) onto a TReDS platform. Multiple financiers banks and NBFCs registered on the platform bid to purchase that invoice at a discount, competing on the discount rate they offer. The MSME accepts the best bid and receives cash immediately, typically within 24–48 hours. When the buyer's payment becomes due, it goes directly to the financier who won the bid.

The core problem TReDS solves: Delayed payments to MSMEs from large buyers are one of the most persistent structural problems in India's economy estimated at a ₹20–25 lakh crore MSME credit gap. TReDS creates a transparent, competitive, electronic marketplace where MSMEs can access working capital against confirmed receivables, without collateral, at rates determined by competitive bidding rather than negotiated bilaterally with a single lender.

The Three Parties in Every TReDS Transaction

1. The MSME Seller the small business that has supplied goods or services and holds an invoice owed by a large buyer. The MSME uploads the invoice to the TReDS platform seeking early payment.

2. The Corporate or Government Buyer the large company, PSU, or government entity that owes payment on the invoice. The buyer's role is to approve (accept) the invoice on the platform, confirming the obligation is genuine and will be paid on the due date. This approval is the foundation of the entire system it converts an MSME's receivable into a confirmed, buyer-acknowledged obligation.

3. The Financier banks and NBFCs registered on the TReDS platform who bid to purchase the approved invoice at a discount. The financier pays the MSME upfront (minus the discount) and receives the full invoice amount from the buyer on the due date.

The critical structural feature: Because the buyer has approved the invoice before it is auctioned, the financier's credit exposure is to the buyer, not the MSME. This is the same structural principle that underlies invoice discounting investments available to individual investors credit risk sits with the large, creditworthy buyer, not the smaller seller.

How a TReDS Transaction Actually Works: Step by Step

Step 1 Invoice upload: The MSME seller uploads the invoice details onto a TReDS platform (RXIL, M1xchange, or Invoicemart), specifying the buyer, invoice amount, and due date.

Step 2 Buyer approval: The corporate or government buyer logs into the platform and approves (accepts) the invoice confirming the amount and due date are correct and the payment obligation is genuine.

Step 3 Auction: Once approved, the invoice becomes available for bidding. Multiple registered financiers (banks, NBFCs) view the approved invoice and submit competing bids each bid specifying the discount rate (effectively, the interest rate) at which they are willing to purchase the invoice.

Step 4 Bid acceptance: The MSME seller reviews the bids and accepts the most favourable one typically the lowest discount rate (best terms for the MSME).

Step 5 Disbursement: The winning financier disburses funds to the MSME's account minus the agreed discount typically within 24 to 48 hours of bid acceptance.

Step 6 Settlement on due date: On the invoice due date, the buyer pays the full invoice amount directly to the financier (not the MSME), completing the transaction.

This entire cycle from invoice upload to MSME receiving funds typically takes 1 to 3 days, compared to the 30–90 day wait the MSME would otherwise face for direct payment from the buyer.

The Three RBI-Licensed TReDS Platforms: RXIL, M1xchange, Invoicemart

India currently has three RBI-licensed TReDS platforms, each with distinct ownership structures and strengths:

| Platform | Promoted By | Key Strength | 2026 Scale Indicator |

|---|---|---|---|

| RXIL (Receivables Exchange of India Ltd) | Joint venture of SIDBI and NSE | Strong institutional backing; deep reach into PSU and NSE-listed buyer ecosystems via SIDBI's MSME network and NSE's market infrastructure | Crossed ₹2 lakh crore in cumulative invoice financing by mid-2025 |

| M1xchange | Promoted by BSE (Bombay Stock Exchange); operated by Mynd Solutions | India's most active platform by transaction volume; robust digital architecture; strong adoption among MSME suppliers to large corporates | Achieved over ₹1 lakh crore annual throughput in FY25-26; cumulative financing crossed ₹2.65 lakh crore |

| Invoicemart (A.TReDS Limited) | Joint venture of Axis Bank and mjunction Services (a JV between SAIL and Tata Steel) | Particularly strong in metro markets and large industrial sectors; broad financier base across public and private banks and NBFCs | Established player with focus on broadening financier participation |

All three platforms operate within the same RBI regulatory framework they are regulated as Trade Receivables Discounting System operators under RBI guidelines, with standardised processes for invoice approval, auction mechanics, and settlement. The ownership differences primarily affect each platform's distribution strengths which buyers, sellers, and financiers it has the strongest existing relationships with rather than the fundamental mechanics of how transactions work.

TReDS Market Size and Growth: The Numbers

The scale of TReDS has grown dramatically and the growth trajectory for 2026 is even steeper following the Union Budget 2026-27 reforms.

| Period | Total Value of Discounted Invoices | Year-on-Year Growth | Notes |

|---|---|---|---|

| FY 2022-23 | ₹76,645 crore | Baseline | Pre-mandate baseline |

| FY 2023-24 | ₹1.38 lakh crore | +62% (transaction volume); +80% (transaction value) | Strong organic growth driven by digital adoption |

| FY 2024-25 (estimated) | ₹1.25–1.30 lakh crore (M1xchange alone) | Continued expansion | M1xchange crossed ₹1 lakh crore annual throughput in FY25-26 |

| FY 2025-26 (projected) | At least ₹1.75 lakh crore (M1xchange alone, projected) | ~40% projected surge | Driven by Union Budget 2026-27 CPSE mandate and GeM integration |

Cumulative figures as of 2025-26: RXIL has surpassed ₹2 lakh crore in cumulative invoice financing; M1xchange has facilitated over ₹2.65 lakh crore cumulatively. Industry-wide projections point to a potential 70% surge in TReDS volumes following the CPSE mandate, given that government and PSU entities previously represented only about 10% of TReDS volume, with the private sector accounting for the remaining 90%.

The structural growth gap: Despite this scale, less than 1% of India's registered MSMEs are currently onboarded to TReDS platforms illustrating both how early-stage this market remains relative to its addressable size, and the magnitude of growth still ahead as onboarding expands.

The Union Budget 2026-27 CPSE Mandate: What Changed

The single most significant TReDS development in 2026 is the Union Budget 2026-27 mandate requiring all Central Public Sector Enterprises (CPSEs) to use TReDS for MSME payments. This is part of a broader four-pillar reform strategy for the TReDS ecosystem:

Pillar 1 Mandatory CPSE participation: All CPSEs are now required to route MSME supplier payments through TReDS platforms. Before this mandate, government and PSU entities represented only roughly 10% of TReDS volume a dramatic underrepresentation given the scale of PSU procurement from MSME suppliers across India.

Pillar 2 GeM Integration: The Government e-Marketplace (GeM) India's procurement platform for government purchases is being integrated with TReDS, improving visibility into financing opportunities arising from government procurement contracts.

Pillar 3 CGTMSE Credit Guarantee Support: The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) is providing enhanced credit guarantee support specifically for invoice discounting transactions on TReDS designed to de-risk financiers and potentially lower financing costs for MSMEs.

Pillar 4 Securitisation of TReDS Receivables: TReDS receivables are being structured as asset-backed securities opening a pathway for institutional capital to access TReDS-originated receivables at scale, similar to how Securitised Debt Instruments (SDIs) package pools of loans for investors.

The combined effect: M1xchange's founder has framed the strategic significance directly positioning TReDS as the settlement platform for CPSEs is expected to drive wider invoice discounting adoption and reinforce TReDS's role in solving India's chronic delayed payment problem for MSMEs. For investors, the practical implication is a substantial increase in PSU-backed, near-sovereign-quality invoice discounting volume flowing through the broader invoice discounting ecosystem.

Can Individual Investors Access TReDS Directly?

No TReDS platforms (RXIL, M1xchange, Invoicemart) are not retail investment platforms. The financiers who bid on TReDS auctions are RBI-regulated banks and NBFCs not individual investors. TReDS is institutional market infrastructure, not a consumer-facing investment product.

This is an important distinction that is often misunderstood. An individual investor cannot log into RXIL or M1xchange and bid on MSME invoices the way a bank treasury desk does.

However, the TReDS ecosystem's growth has direct relevance for individual investors for two reasons:

1. TReDS sets the benchmark pricing for invoice discounting. TReDS rates currently range from approximately 7% to 11% per annum for MSMEs, driven down by competitive bidding among regulated financiers. This is the institutional benchmark for what large corporate and PSU buyer credit "costs" in the invoice financing market directly informing the yields available on retail invoice discounting platforms for comparable buyer quality.

2. Some invoice discounting platforms source deal flow informed by or adjacent to the TReDS ecosystem. While retail platforms like Ultra operate independently of the TReDS auction mechanism itself, the same underlying dynamic large corporate and PSU buyers with approved payment obligations to MSME suppliers is the foundation of the invoice discounting deals offered to individual investors. The CPSE mandate's expansion of PSU-backed receivables strengthens the overall supply and quality of this underlying opportunity set across the broader invoice financing market.

TReDS vs Fintech Invoice Discounting Platforms: The Investor's View

| Dimension | TReDS (RXIL, M1xchange, Invoicemart) | Retail/HNI Invoice Discounting Platforms |

|---|---|---|

| Who can participate as a financier | RBI-regulated banks and NBFCs only | Individual investors, typically from ₹10,000–₹25,000 minimum |

| Mechanism | Auction-based multiple financiers bid competitively on each invoice | Curated platform pre-screens deals and offers fixed yield to investors |

| Typical rates | 7%–11% (MSME cost of financing, driven down by competition) | 10%–15% (investor yield, varies by buyer tier) |

| Regulatory framework | RBI-licensed Market Infrastructure Institution | Varies curated alternative investment marketplace or NBFC-affiliated structures |

| Buyer approval requirement | Mandatory buyer must approve invoice before auction | Platform-dependent GSTN verification and buyer disclosure vary by platform |

| Settlement speed to MSME | 24–48 hours after bid acceptance | Platform-dependent |

The rate differential explained: TReDS rates (7–11%) represent what MSMEs pay to access financing through competitive institutional bidding this is the MSME's cost of capital. Retail invoice discounting platforms offer investors yields of 10–15% because the underlying economics include the platform's curation, the specific buyer-tier risk premium, and the structure through which retail capital is deployed these are not directly comparable rates, but the TReDS rate range is a useful reference point for understanding where large-buyer invoice financing is priced at the institutional level.

What the TReDS Growth Story Means for Invoice Discounting Investors

For investors in invoice discounting whether through Ultra or other platforms the TReDS growth story matters for three structural reasons:

1. Validation of the underlying asset class. TReDS demonstrates that invoice discounting against large corporate and PSU buyer obligations is a mainstream, RBI-regulated, institutionally-validated financing mechanism not a niche or experimental product. Banks and NBFCs deploying tens of thousands of crores through TReDS auctions reflects institutional confidence in this credit type.

2. Expansion of PSU-backed deal supply. The CPSE mandate is expected to drive a meaningful increase in PSU-backed receivables flowing through the broader invoice financing ecosystem. PSU buyers central public sector enterprises with strong balance sheets and government backing represent some of the lowest-risk buyer profiles in invoice discounting. As this mandate takes effect through 2026 and beyond, the pool of high-quality, PSU-backed invoice discounting opportunities is structurally expanding.

3. Rate benchmark stability. With TReDS rates for MSMEs in the 7-11% range and growing competitive participation from financiers, the overall invoice financing market is becoming more liquid and transparent. This benefits investors by providing clearer reference points for what constitutes a fair yield for a given buyer-quality tier.

Risks and Limitations in the TReDS Ecosystem

A balanced view of TReDS requires acknowledging its current limitations:

MSME adoption remains very low. Less than 1% of India's registered MSMEs are onboarded to TReDS platforms. The mandate addresses the buyer side (CPSEs must participate) but does not automatically solve MSME-side adoption challenges many smaller enterprises struggle with the documentation and digital readiness required for KYC and onboarding.

TReDS does not solve all MSME working capital needs. TReDS specifically addresses invoice discounting against approved receivables from large buyers it does not address other working capital needs such as inventory financing, pre-shipment finance, or term loans for capacity expansion.

Reliance on mandates raises sustainability questions. While the CPSE mandate will mechanically increase TReDS volumes, some industry observers note that growth driven primarily by regulatory mandate (rather than organic adoption) raises questions about whether the underlying behavioural shift MSMEs and buyers genuinely preferring TReDS for its competitive pricing is occurring at the pace the headline volume numbers might suggest.

Growth rate is moderating. TReDS saw exponential early growth (volumes more than tripling between 2020-2022, with 113% year-on-year growth in 2021), but growth rates have moderated toward approximately 32% by 2025 indicating a maturing market, even before accounting for the new CPSE-driven surge.

Ultra's Position: Why the TReDS Mandate Matters for Your Portfolio

Applying the audit principle Ultra's specific view:

The TReDS CPSE mandate is the single most important structural development for invoice discounting investors in 2026 not because it gives individual investors direct TReDS access (it does not), but because it validates and expands the underlying opportunity set that platforms like Ultra curate from.

The mandate's core effect bringing CPSEs, which previously represented only ~10% of TReDS volume, into mandatory participation means a structurally larger pool of PSU-backed receivables is moving through India's formal invoice financing ecosystem. PSU buyers are precisely the buyer tier that delivers the lowest-risk, most "near-sovereign" invoice discounting opportunities for individual investors.

What this means practically for HNI investors:

The growing supply of PSU-backed invoice discounting deals a direct consequence of the CPSE mandate supports Ultra's continued ability to offer deals on Tier 1 buyer profiles (PSUs, large listed corporates) at the 10–13% yield range, with the sub-1% historical credit loss rate Ultra has maintained on this buyer tier. As the CPSE mandate matures through 2026 and 2027, investors should expect the available pool of PSU-backed deals to expand a genuine structural tailwind, not a marketing narrative.

What Ultra would not overstate: The CPSE mandate does not mean individual investors gain access to TReDS auction rates (7-11%) directly retail invoice discounting yields (10-15%) reflect a different access structure. Nor does the mandate eliminate the MSME adoption challenges that remain real limitations on how quickly the broader ecosystem scales. The mandate is a supply-side tailwind for deal quality and quantity not a guarantee of specific yield levels.

For a complete guide to invoice discounting returns and how PSU buyer deals fit into a portfolio, read: Invoice Discounting in India: Returns, Risks & How HNIs Invest and How HNIs Are Using Invoice Discounting in 2026.

FAQs

Q1. What is TReDS and how does it work?

TReDS (Trade Receivables Discounting System) is an RBI-regulated electronic platform that allows MSMEs to convert unpaid invoices from large corporate or government buyers into immediate cash. The buyer first approves the invoice, confirming the payment obligation. The approved invoice is then auctioned to a pool of RBI-regulated banks and NBFCs, who bid competitively to purchase it at a discount. The MSME accepts the best bid and receives funds typically within 24-48 hours, while the buyer pays the financier directly on the original due date.

Q2. What are the three TReDS platforms in India?

India has three RBI-licensed TReDS platforms: RXIL (Receivables Exchange of India Ltd), a joint venture of SIDBI and NSE; M1xchange, promoted by BSE and operated by Mynd Solutions, India's most active platform by volume; and Invoicemart (A.TReDS Limited), a joint venture of Axis Bank and mjunction Services. All three operate under the same RBI regulatory framework for invoice discounting.

Q3. Can individual investors invest through TReDS platforms?

No. TReDS platforms are institutional market infrastructure only RBI-regulated banks and NBFCs can participate as financiers bidding on invoices. Individual investors cannot directly access RXIL, M1xchange, or Invoicemart as investment platforms. However, the broader invoice discounting ecosystem that retail and HNI platforms draw from shares the same underlying principle large corporate and PSU buyer obligations to MSME suppliers.

Q4. What is the Union Budget 2026-27 CPSE mandate for TReDS?

The Union Budget 2026-27 mandated that all Central Public Sector Enterprises (CPSEs) must use TReDS for MSME supplier payments. Previously, government and PSU entities represented only about 10% of TReDS volume, with private sector buyers accounting for 90%. This mandate, alongside GeM integration, CGTMSE credit guarantee support, and securitisation of TReDS receivables, is projected to drive a significant surge in TReDS volumes with some platforms projecting up to a 40-70% increase.

Q5. What interest rates do MSMEs pay on TReDS?

TReDS financing rates for MSMEs currently range from approximately 7% to 11% per annum, driven down through competitive bidding among RBI-regulated banks and NBFCs. This is the institutional cost of financing for MSMEs accessing TReDS a different rate structure from the 10-15% yields available to individual investors on retail invoice discounting platforms, which reflect a different access mechanism and risk-return structure.

Q6. How big is the TReDS market in India in 2026?

TReDS has grown substantially: total discounted invoice value rose from ₹76,645 crore in FY2022-23 to ₹1.38 lakh crore in FY2023-24 (62% volume growth, 80% value growth). RXIL has surpassed ₹2 lakh crore in cumulative financing, and M1xchange has facilitated over ₹2.65 lakh crore cumulatively, achieving over ₹1 lakh crore in annual throughput in FY25-26. Industry projections following the CPSE mandate point to potential growth of 40-70% in the coming fiscal year. Despite this scale, less than 1% of India's registered MSMEs are currently onboarded.

Disclaimer

This article is for informational and educational purposes only and does not constitute investment advice. TReDS platform data, volumes, and rates are based on publicly available information from RBI, SIDBI, and platform disclosures as of mid-2026, and are subject to change. TReDS platforms are institutional infrastructure and not directly accessible to individual investors. Please conduct your own due diligence before investing in any invoice discounting product.