How to Earn 12% Fixed Returns in India: Realistic Options Explained (2026)

06 April 2026 · Sachin Gadekar

A no-nonsense guide to earning 12% fixed returns in India through realistic, regulated investment options without touching equity markets or locking up money for years.

Is 12% Return Realistic in India?

Every investor wants higher returns. But when you search "how to earn 12% returns in India," most results either push you toward equity mutual funds (which are market-linked and volatile) or vague suggestions that don't hold up in practice.

This guide is different. We focus specifically on fixed and near-fixed return options instruments where the return is predictable, the tenure is defined, and the outcome is not dependent on whether the Sensex goes up or down next week. And we answer honestly: is 12% actually achievable without taking excessive risk?

The short answer is yes: but only through the right asset classes, and only if you know where to look.

Yes but with an important caveat: 12% fixed returns do not come from traditional, government-backed instruments. Bank FDs currently offer 6.5–7.5%, RBI Floating Rate Bonds offer 8.05%, and even the best corporate FDs from AAA-rated companies top out around 8.5–9%.

To reach 12%, you need to move into alternative fixed income a category of regulated, structured financial instruments that offer higher yields in exchange for slightly higher risk than bank deposits. These include invoice discounting, high-yield corporate bonds, asset leasing, and structured debt products.

The key distinction from equity: your return is pre-agreed. You know what you will earn before you invest. There is no market price risk, no NAV fluctuation, and no dependence on how a company's stock performs.

The risk is primarily credit risk the risk that the borrower defaults. This is why platform selection, due diligence, and diversification matter enormously in this space.

Why Traditional Investments Fall Short

| Instrument | Typical Return | Tenure | Safety |

|---|---|---|---|

| Bank FD (SBI/HDFC) | 6.5%–7.5% | 1–5 years | Very High (insured up to ₹5L) |

| RBI Floating Rate Bonds | 8.05% | 7 years | Sovereign |

| Senior Citizen Savings Scheme | 8.2% | 5 years | Sovereign |

| Corporate FD (AAA-rated) | 8%–9% | 1–3 years | High |

| Debt Mutual Funds | 7%–8.5% | Flexible | Moderate |

| PPF | 7.1% | 15 years | Sovereign |

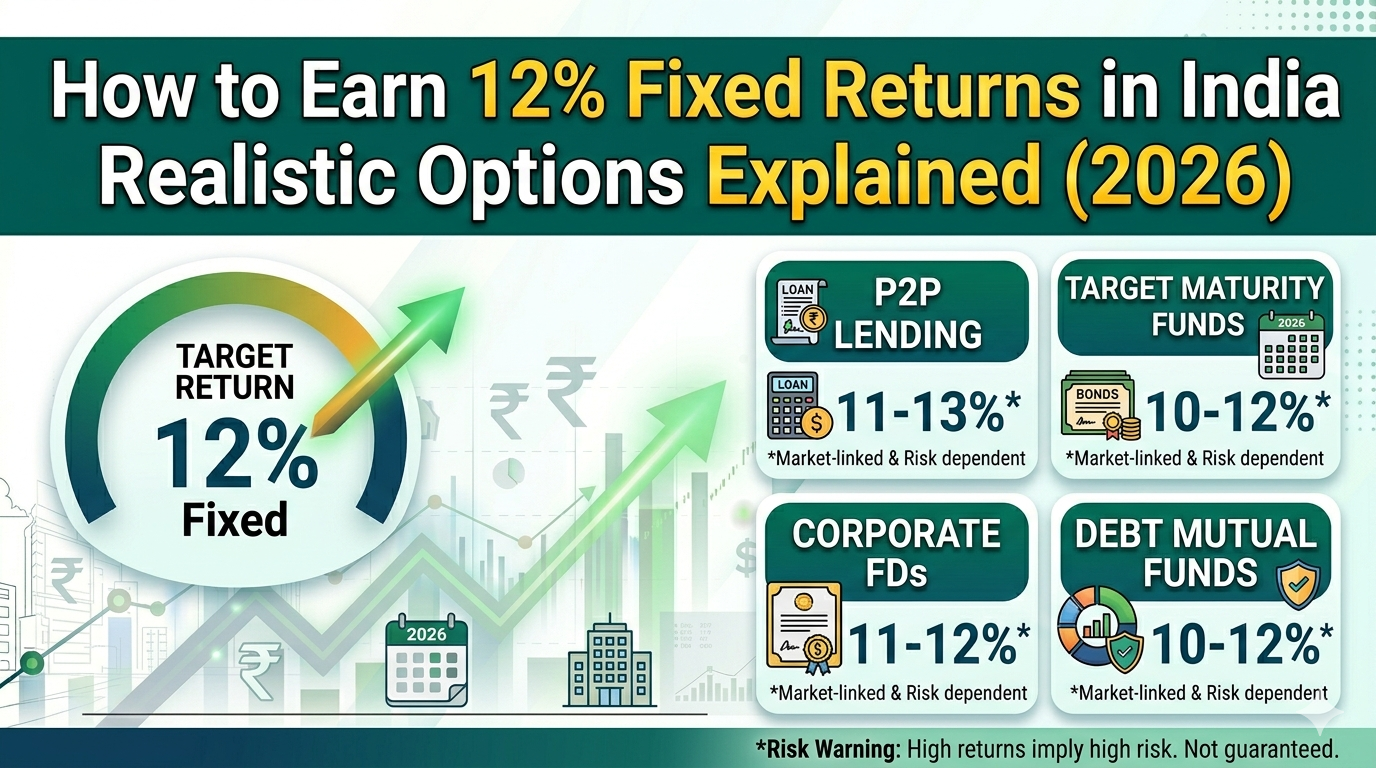

Option 1: Invoice Discounting

Typical Returns: 10%–15% p.a.

Invoice discounting is one of the most accessible and transparent ways to earn 12%+ fixed returns in India. Here is how it works:

A business raises an invoice to a large corporate client — say, ₹10 lakhs payable in 60 days. Instead of waiting, the business lists this invoice on a platform like Ultra. You, as an investor, fund the invoice at a slight discount (say ₹9.80 lakhs). When the corporate client pays on day 60, you receive the full ₹10 lakhs — earning ₹20,000 on a 60-day investment, which annualises to approximately 12–13%.

The key to safety here is the payer quality — if the invoice is backed by a large, listed, or government-backed corporate, the credit risk is low.

Why it works for 12% targets:

Returns are pre-agreed and fixed — you know your return before investing

Tenures are short (30–90 days) — capital rotates fast and compounds well

Non-market linked — no correlation with stock market movements

Platforms like ultra curate and underwrite deals before listing them

Risk to watch: Default by the invoice payer. Mitigate by diversifying across multiple invoices and preferring deals backed by well-rated corporates.

Option 2: High-Yield Corporate Bonds and NCDs

Typical Returns: 10%–13% p.a.

Not all corporate bonds are created equal. While AAA-rated bonds from blue-chip companies yield 8–9%, high-yield bonds from AA, A, or BBB-rated issuers can offer 10–13% and still carry investment-grade or near-investment-grade credit ratings.

Non-Convertible Debentures (NCDs) are the most common form these take in India. They are listed on exchanges, regulated by SEBI, and pay fixed coupon interest on a defined schedule (monthly, quarterly, or annually).

What makes this realistic at 12%:

Mid-sized NBFCs, real estate companies, and infrastructure firms regularly issue NCDs at 11–13%

Listed NCDs offer secondary market liquidity you are not locked in until maturity

Curated platforms that pre-screen issuers reduce the burden of individual credit analysis

Risk to watch: Issuer credit quality a higher yield always means higher credit risk. Stick to rated instruments and avoid chasing the highest possible coupon without examining the issuer's financials.

Option 3: Asset Leasing

Typical Returns: 10%–14% p.a.

Asset leasing is a simple concept: you co-invest in a physical asset a truck, a piece of machinery, a medical device and earn a share of the lease rental that businesses pay to use it.

The asset is leased to a company for a fixed period (typically 2–4 years). You receive monthly lease payments as your return. At the end of the lease, the asset is either sold or re-leased, and you receive your principal back.

Why it reaches 12%:

Returns combine rental yield + residual asset value

Asset-backed nature provides a layer of security even in default, the asset can be recovered and sold

Non-market correlated returns a truck's lease payments don't fluctuate with the Nifty

Risk to watch: Asset depreciation and lessee default. Choosing well-maintained assets leased to creditworthy companies significantly reduces both risks.

Option 4: P2P Lending

Typical Returns: 10%–18% p.a.

Peer-to-peer (P2P) lending platforms regulated by the RBI connect individual lenders (investors) with borrowers directly. Returns can be among the highest in the fixed income spectrum but so can the risk.

The RBI-regulated P2P lending space in India includes platforms, where you can earn 12–18% by lending to vetted borrowers. Returns are paid as monthly EMIs that include both principal and interest.

Why it can reach 12%:

Direct lending cuts out the bank as intermediary, increasing the yield to the lender

Diversification across hundreds of borrowers reduces individual default impact

RBI regulation provides some framework protection

Risk to watch: The highest-return category here. Borrower defaults are more common than in invoice discounting or corporate bonds. Strictly diversify never put more than 1–2% of your P2P portfolio into a single borrower.

Option 5: Securitised Debt Instruments (SDIs)

Typical Returns: 10%–13% p.a.

SDIs are a relatively newer alternative investment category in India, popularised by platforms like Grip Invest. A pool of receivables retail loans, lease payments, or business debt is securitised and sold as a structured instrument to investors.

You effectively invest in a basket of underlying cash flows, not a single borrower. This pooling effect provides natural diversification, and returns are typically fixed and paid out periodically.

Why it reaches 12%:

Pooled structure reduces concentration risk versus single-borrower lending

Returns are legally structured and predictable

SEBI oversight provides regulatory assurance

Risk to watch: Complexity these are not as easy to evaluate as a simple invoice or NCD. Rely on platforms with transparent disclosure of the underlying asset pool quality.

Comparison: Which Option Is Right for You?

| Option | Typical Return | Tenure | Minimum Investment | Liquidity | Risk Level | Best For |

|---|---|---|---|---|---|---|

| Invoice Discounting | 10%–15% | 30–90 days | ₹25,000–₹1L | Low (locked till maturity) | Low–Moderate | Short-term, high-rotation investors |

| High-Yield Corporate Bonds / NCDs | 10%–13% | 1–5 years | ₹10,000–₹1L | Moderate (secondary market) | Moderate | Investors wanting regular coupon income |

| Asset Leasing | 10%–14% | 2–4 years | ₹20,000–₹1L | Low (fixed tenure) | Low–Moderate | Investors wanting tangible asset-backed income |

| P2P Lending | 12%–18% | 3–36 months | ₹500–₹5,000 per loan | Low–Moderate | Moderate–High | Risk-tolerant investors seeking highest yield |

| Securitised Debt (SDIs) | 10%–13% | 6–36 months | ₹10,000–₹1L | Low | Moderate | Investors wanting diversified debt exposure |

What to Watch Out For

Earning 12% fixed returns in India is genuinely achievable — but there are landmines to avoid:

1. Unregulated or opaque platforms Only invest through platforms that are SEBI-registered (for bonds and SDIs), RBI-registered (for P2P), or operate through structured, audited deal formats. Avoid any platform that cannot clearly explain where your money goes and how it is protected.

2. Chasing the highest yield without reading the credit A 20% "guaranteed" return from an unknown NBFC is not the same as a 12% return from a vetted invoice backed by a listed corporate. Higher yield always means higher risk — the question is whether that risk is worth taking and whether it has been disclosed to you.

3. Concentrating into a single deal or issuer Diversification is the single most effective risk management tool in this space. Split your capital across multiple invoices, multiple bonds, or multiple borrowers. Never put more than 5–10% of your alternative fixed income allocation into a single deal.

4. Ignoring taxation Returns from invoice discounting, bonds, and P2P lending are taxed as per your income slab — which at the 30% bracket effectively reduces a 12% gross return to ~8.4% post-tax. Factor this into your net return expectations before investing.

5. Confusing short-tenure with liquidity A 60-day invoice is not liquid — you cannot redeem it early if you need the money. Plan your cash flows before locking in, regardless of tenure.

How to Get Started

The simplest path to earning 12% fixed returns in India:

Step 1: Define your allocation Decide how much of your overall portfolio you want to allocate to alternative fixed income. A common starting point for HNIs is 15–25% of the fixed income portion of the portfolio.

Step 2: Choose your primary instrument Start with invoice discounting or high-yield bonds if you are new to alternative investments — they are the most transparent and regulated. Add asset leasing and SDIs as you gain comfort.

Step 3: Diversify from day one Split your initial allocation across at least 5–10 different deals or instruments. Never put everything into one deal, one issuer, or one platform.

Step 4: Use a curated platform Platforms like Ultra pre-screen deals, conduct credit due diligence, and present only vetted opportunities — saving you the effort of evaluating every issuer from scratch.

Step 5: Reinvest returns The compounding effect is strongest in short-tenure instruments like invoice discounting. Reinvesting your 60-day returns into new deals immediately is how 12% annualised becomes genuinely powerful over 12–24 months.

FAQs

Q1. Is it really possible to earn 12% fixed returns in India without equity?

Yes. Invoice discounting, high-yield NCDs, and asset leasing regularly deliver 10–14% annualised returns without any equity market exposure. The key is choosing the right platform and diversifying across deals.

Q2. Are these investments safe?

They are safer than equity but carry more risk than bank FDs. The primary risk is credit risk — the possibility that the borrower or invoice payer defaults. This can be managed through careful platform selection and diversification.

Q3. What is the minimum amount needed to start earning 12% returns?

You can start with as little as ₹25,000 in invoice discounting. Most high-yield bond and asset leasing platforms have minimums of ₹10,000–₹1 lakh. For meaningful diversification, a starting capital of ₹2–5 lakhs is ideal.

Q4. How is 12% taxed in India?

Returns from invoice discounting and P2P lending are treated as interest income and taxed at your income slab rate. Listed NCD coupon income is also taxed as interest. Factor in your effective tax rate to calculate post-tax returns.

Q5. How does 12% fixed compare to equity mutual funds?

Equity mutual funds may deliver 12–15% over long periods, but with significant volatility and no guaranteed return. Fixed alternatives at 12% offer predictability — you know your return before investing. The right choice depends on your risk tolerance and investment horizon.

Q6. Which platform should I use to invest?

Look for platforms that are SEBI or RBI registered, have transparent deal disclosure, perform credit due diligence, and have a track record of timely payouts. Ultra offers curated access to invoice discounting, bonds, and other fixed income instruments with full transparency.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Returns mentioned are indicative and based on current market conditions. All investments carry risk. Please consult a registered financial advisor before investing.

Explore curated fixed income opportunities delivering 10–15% returns at ultra vetted deals, transparent terms, and no market risk.