Best Passive Income Investments in India Delivering 10%+ Returns (2026)

07 April 2026 · Sachin Gadekar

A focused guide to the best investment-based passive income options in India that consistently deliver 10% or more — without equity risk, complex strategies, or locking up money for decades.

What Counts as Passive Income from Investments?

Ask ten people what passive income means in India and you will get ten different answers — rental properties, dividend stocks, YouTube channels, online courses. While all of these are legitimate, this guide is different. We focus exclusively on investment-based passive income — instruments where you deploy capital and earn regular, predictable returns without active involvement.

More specifically, we focus on options that deliver 10% or more annually — a threshold that eliminates most traditional options (bank FDs, PPF, government bonds) and pushes you into the more interesting territory of alternative fixed income.

Here is a ranked, honest comparison of the best passive income investment options in India for 2026 that clear the 10% bar.

For the purposes of this guide, passive income from investments means capital you deploy once, and that generates recurring returns with little or no ongoing effort. This includes:

Interest income from bonds, NCDs, and invoice discounting

Lease rentals from asset leasing investments

Distribution income from REITs

Dividend income from stocks

It excludes active income streams that require ongoing effort content creation, rental property management, freelancing even if those are called "passive" elsewhere.

Why 10% Is the Right Benchmark

10% is not an arbitrary number. Here is why it matters:

Inflation in India has historically averaged 5–6% annually. An investment that earns less than 7–8% is effectively eroding your purchasing power over time.

Bank FDs currently offer 6.5–7.5% the most common passive income instrument for most Indian investors.

10%+ represents the threshold where you start genuinely outpacing inflation, generating real wealth, and building meaningful passive income on a reasonable capital base.

To illustrate: on a ₹50 lakh corpus, the difference between 7% and 11% returns is ₹3.5 lakh vs ₹5.5 lakh in annual income a ₹2 lakh gap every year, or ₹20 lakhs over a decade, from the same corpus.

That gap is exactly why understanding your options above 10% matters.

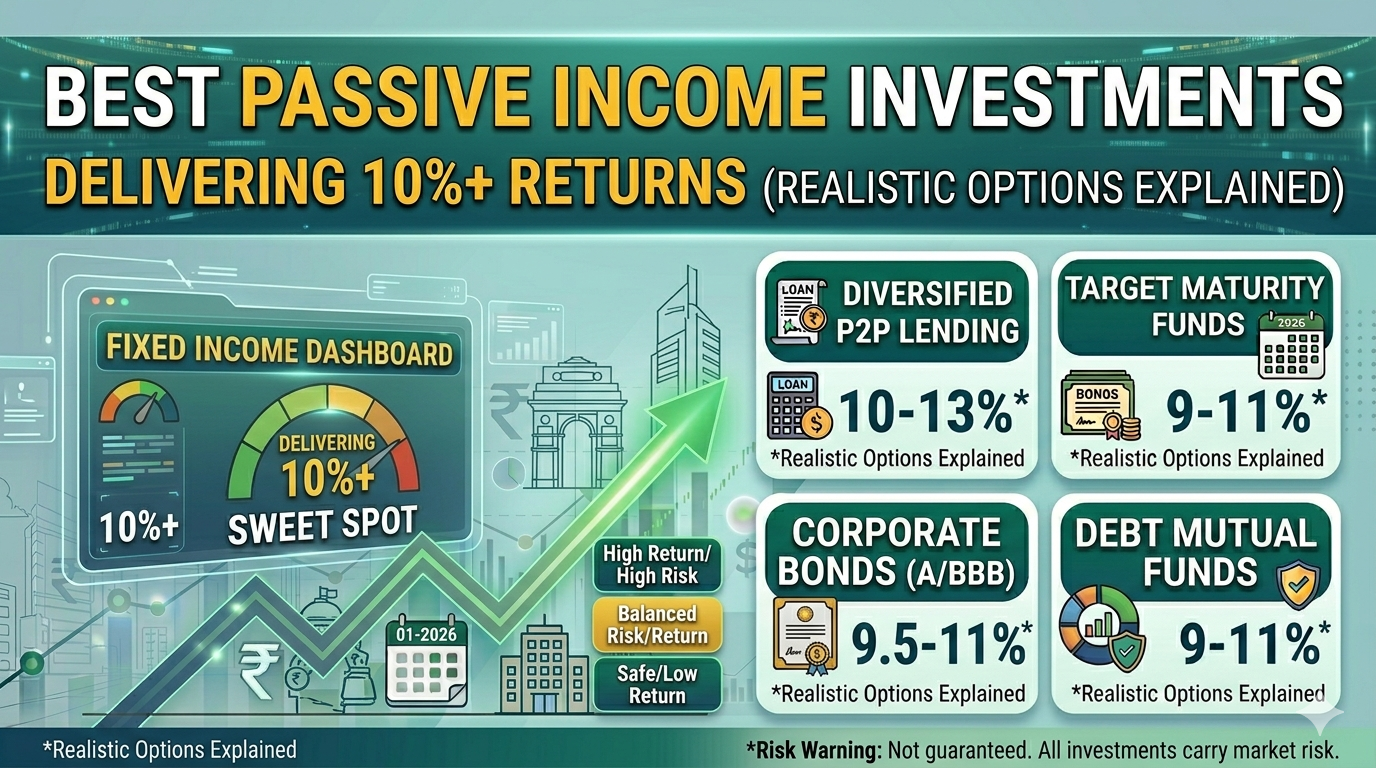

1. Invoice Discounting — 10% to 15% p.a.

Best for: Short-term investors wanting high, predictable returns

Invoice discounting is the standout passive income instrument for investors who want short tenures, predictable returns, and no market exposure. Businesses raise invoices against large corporates and list them on platforms like Ultra. You fund the invoice at a discount and earn the margin when the corporate pays — typically within 30–90 days.

Why it makes the 10%+ cut:

Returns are pre-agreed and fixed before you invest typically 10–15% annualised

Short tenures mean rapid capital recycling your money doesn't sit idle

Returns are backed by real business transactions, not market sentiment

Platforms pre-screen deals for credit quality

Income frequency: Lump sum at maturity (every 30–90 days)

Key risk: Invoice payer default. Mitigated by investing in invoices backed by large, rated corporates and diversifying across multiple deals.

Minimum investment: ₹25,000–₹1 lakh depending on platform

2. High-Yield Corporate Bonds and NCDs — 10% to 13% p.a.

Best for: Investors wanting regular coupon income over 1–5 years

Not all corporate bonds yield the same. While AAA-rated bonds from blue chips offer 8–9%, bonds from AA, A, or BBB-rated issuers — especially NBFCs, real estate companies, and infrastructure firms — regularly offer 10–13%. Non-Convertible Debentures (NCDs) are the most common form.

Why it makes the 10%+ cut:

Coupon payments are fixed you know your income before investing

Listed NCDs provide secondary market liquidity — you can exit before maturity if needed

SEBI-regulated, credit-rated instruments offer structured safety compared to unrated alternatives

Platforms like BondScanner, Jiraaf, Wint Wealth, Grip Invest, and curate pre-screened high-yield bonds

Income frequency: Monthly, quarterly, or annual coupon payments

Key risk: Issuer credit risk if the company faces financial stress, coupon or principal repayment could be delayed. Stick to rated instruments and diversify across issuers.

Minimum investment: ₹10,000–₹1 lakh

3. Asset Leasing — 10% to 14% p.a.

Best for: Investors wanting asset-backed, tangible passive income

Asset leasing is one of the more elegant passive income structures available in India today. You co-invest in a physical asset a truck, excavator, piece of medical equipment, or solar panel array — and earn a monthly share of the lease rental that a company pays to use it.

Why it makes the 10%+ cut:

Returns combine rental yield and residual asset value often reaching 12–14% annualised

Asset-backed security the physical asset can be recovered and sold in a default scenario

Non-market correlated a lease rental has nothing to do with Nifty movements

Monthly payouts make it excellent for passive income planning

Income frequency: Monthly lease payments one of the best options for regular passive income

Key risk: Asset depreciation and lessee default. Choose platforms that conduct asset quality checks and work with creditworthy lessees.

Minimum investment: ₹20,000–₹1 lakh

4. Securitised Debt Instruments (SDIs) — 10% to 13% p.a.

Best for: Investors wanting diversified debt exposure in a single instrument

SDIs pool multiple receivables — retail loans, lease payments, or trade receivables — and package them into a structured instrument that investors can buy. Instead of one borrower, you are exposed to a basket of borrowers, which provides natural diversification.

Why it makes the 10%+ cut:

Pooled structure reduces concentration risk significantly

Returns are fixed and paid periodically — typically 10–13% annualised

SEBI oversight provides regulatory framework

Available through platforms like Grip Invest and Ultra

Income frequency: Monthly or quarterly distributions

Key risk: Complexity — evaluating the quality of the underlying asset pool requires more diligence than a single-issuer bond. Rely on platforms with transparent pool disclosure.

Minimum investment: ₹10,000–₹1 lakh

5. P2P Lending — 12% to 18% p.a.

Best for: Higher risk-tolerance investors seeking maximum yield

Peer-to-peer lending connects you directly with individual borrowers through RBI-regulated platforms. You become the lender and earn the interest that would otherwise go to a bank. Returns are the highest in this list — but so is the risk.

Why it makes the 10%+ cut:

Returns of 12–18% are among the highest available in structured passive income

Monthly EMI payouts provide regular cash flow

RBI regulation provides an operating framework and borrower verification standards

Income frequency: Monthly EMIs (includes principal + interest)

Key risk: Higher default risk than other instruments on this list. Individual borrowers default more frequently than corporate entities. Strict diversification across hundreds of borrowers is non-negotiable.

Minimum investment: ₹500–₹5,000 per borrower

6. REITs and SM REITs — 8% to 10% distribution yield

Best for: Investors wanting real estate income with stock-exchange liquidity

Real Estate Investment Trusts (REITs) and the newer Small and Medium REITs (SM REITs) distribute rental income from commercial properties office buildings, malls, warehouses to unit holders on a quarterly basis. We include them here as they sit just at or slightly below the 10% threshold, but offer unique benefits.

Why they are worth mentioning:

Distribution yields of 8–10% are competitive with high-yield bonds and come with potential capital appreciation

Exchange-listed you can buy and sell on BSE/NSE like a stock

Regulatory protection SEBI oversight ensures 90% of income distributed to unit holders

SM REITs (like PropShare Platina and Titania) offer access to specific Grade A+ office assets

Income frequency: Quarterly distributions

Key risk: Minimum investment in SM REITs is ₹10 lakhs per unit making them accessible only to HNIs. Large REITs (Embassy, Mindspace, Nexus) are more accessible with smaller lot sizes.

Minimum investment: ₹10,000+ for large REITs; ₹10 lakhs for SM REITs

7. Dividend Stocks — Variable (typically 2% to 8%)

Best for: Long-term investors building a compounding equity income stream

We include dividend stocks for completeness — but with an important caveat. Most Indian dividend stocks do not consistently clear the 10% dividend yield threshold. Blue-chip payers like ITC, Coal India, and ONGC offer 4–7% dividend yields, which is meaningful but falls short of our benchmark.

Dividend stocks are better understood as a long-term wealth compounder — total return (dividend + capital appreciation) over 10+ years can be excellent. But as a pure passive income instrument targeting 10%+ in the near term, they generally do not qualify.

Include in your portfolio only if: You have a long time horizon and are comfortable with equity market volatility alongside the dividend income.

Master Comparison: All Options at a Glance

| Investment Option | Return Range | Income Frequency | Min. Investment | Tenure | Risk Level | Clears 10% Bar? |

|---|---|---|---|---|---|---|

| Invoice Discounting | 10%–15% p.a. | At maturity (30–90 days) | ₹25,000–₹1L | 30–90 days | Low–Moderate | Yes |

| High-Yield Corporate Bonds / NCDs | 10%–13% p.a. | Monthly / Quarterly / Annual | ₹10,000–₹1L | 1–5 years | Moderate | Yes |

| Asset Leasing | 10%–14% p.a. | Monthly | ₹20,000–₹1L | 2–4 years | Low–Moderate | Yes |

| Securitised Debt Instruments (SDIs) | 10%–13% p.a. | Monthly / Quarterly | ₹10,000–₹1L | 6–36 months | Moderate | Yes |

| P2P Lending | 12%–18% p.a. | Monthly EMIs | ₹500–₹5,000 per loan | 3–36 months | Moderate–High | Yes (higher risk) |

| REITs / SM REITs | 8%–10% p.a. | Quarterly | ₹10,000–₹10L | Open-ended | Low–Moderate | Borderline |

| Dividend Stocks | 2%–8% yield | Quarterly / Annual | ₹500+ | Open-ended | Moderate–High | No (on yield alone) |

| Bank FD | 6.5%–7.5% p.a. | Monthly / Quarterly / At maturity | ₹1,000+ | 1–5 years | Very Low | No |

Which Options Actually Deliver 10%+ Consistently?

Based on the comparison above and competitor platform data from, here is a realistic assessment:

Consistently above 10%:

Invoice discounting (when backed by quality corporates, platforms like altGraaf and ultra routinely offer 10–14%)

Asset leasing (Grip Invest and altGraaf regularly list opportunities at 10–14%)

High-yield NCDs (Jiraaf and Wint Wealth list 10–13% instruments regularly)

Sometimes above 10%, depends on deal quality:

SDIs (Grip Invest offers these; returns vary by pool quality)

P2P lending (highest yield but most variable — depends on borrower quality and defaults)

Rarely above 10% on distribution yield alone:

REITs (8–10% is the realistic range; SM REITs at the top end)

Dividend stocks (yield rarely exceeds 7–8% for quality Indian companies)

The clear winner for consistent 10%+ passive income with reasonable risk is the invoice discounting + high-yield bonds + asset leasing combination — available through curated platforms like ultra.

How to Build a 10%+ Passive Income Portfolio

| Instrument | Suggested Allocation | Expected Return | Income Frequency | Purpose |

|---|---|---|---|---|

| Invoice Discounting | 35% | 11%–14% | Every 30–90 days | High yield, rapid capital rotation |

| High-Yield Corporate Bonds / NCDs | 35% | 10%–12% | Monthly / Quarterly | Regular coupon income, medium tenure |

| Asset Leasing | 20% | 11%–13% | Monthly | Asset-backed stability, monthly payouts |

| REITs (large listed) | 10% | 8%–10% | Quarterly | Real estate exposure with liquidity |

FAQs

Q1. What is the best passive income investment in India for 10%+ returns?

Invoice discounting, high-yield NCDs, and asset leasing are the most consistent passive income options delivering 10%+ in India. They are non-market linked, have defined tenures, and pay predictable returns. Platforms like Ultra offer curated access to all three.

Q2. Can I really earn 10% passive income without stock market risk?

Yes. Invoice discounting, bonds, and asset leasing are all non-market linked instruments. Returns are based on business transactions and credit obligations, not stock prices or index movements.

Q3. How much money do I need to start earning 10%+ passive income?

You can start with as little as ₹25,000 in invoice discounting or ₹10,000 in bonds. For a meaningful monthly passive income (say ₹20,000–₹30,000/month), you would need a corpus of approximately ₹25–35 lakhs deployed at 10–12%.

Q4. Is 10%+ passive income taxable in India?

Yes. Income from invoice discounting, bonds, and asset leasing is taxed as interest income under your applicable slab rate. At the 30% bracket, your post-tax return on a 13% gross yield would be approximately 9.1%. Factor this into your planning.

Q5. Which is better — invoice discounting or bonds for passive income?

It depends on your preference. Invoice discounting offers higher yields and shorter tenures (30–90 days) but pays in lump sums. Bonds offer regular monthly or quarterly coupon payments but lock in capital for 1–5 years. Many investors use both together for a diversified income stream.

Q6. Are these investments safe?

They are safer than equity but carry more risk than bank FDs. The primary risk is credit risk the borrower or invoice payer defaulting. This is manageable through platform selection, credit due diligence, and diversification across multiple deals.

Disclaimer

This article is for informational purposes only and does not constitute investment advice. Returns are indicative based on current market conditions. All investments carry risk. Please consult a registered financial advisor before investing.

Start building your 10%+ passive income portfolio today. Explore curated invoice discounting, Pre IPO, and asset leasing opportunities at ultra pre-screened deals, full transparency, and no market risk.