How to Build a ₹1 Crore Fixed Income Portfolio in India (2026)

17 June 2026 · Sachin Gadekar

A complete, allocation-by-allocation guide to building a ₹1 crore fixed income portfolio in India in 2026, covering invoice discounting, corporate bonds, asset leasing, SDIs, REITs, AIFs, and the liquidity buffer, with exact post-tax income calculations and Ultra's specific recommendation.

₹1 crore is a meaningful threshold in Indian wealth management. It is large enough to access AIFs (SEBI's ₹1 crore minimum for Category I, II, and III), to negotiate bulk FD rates, and to build genuine diversification across 6-8 instruments rather than concentrating in 1-2. It is also small enough that the difference between a thoughtfully constructed portfolio and a default FD-heavy allocation translates into a very real, very large rupee gap in annual income.

This article builds that portfolio allocation by allocation, with exact post-tax income calculations at each step for an investor with ₹1 crore in surplus capital to deploy into fixed income in 2026.

The default approach most of ₹1 crore sitting in bank FDs at 6.5-6.85% generates approximately ₹4.5-4.7 lakhs post-tax annually at the 30% bracket. The constructed portfolio in this article generates ₹7.8-8.5 lakhs post-tax annually a difference of roughly ₹3.2-3.8 lakhs per year, or ₹32-38 lakhs over 10 years before compounding. That gap is the entire argument for reading further.

The Starting Point: What "Fixed Income" Actually Means in 2026

For most of the last two decades, "fixed income" in an Indian investor's portfolio meant exactly two things: bank FDs and, for the more sophisticated, debt mutual funds. In 2026, that definition is meaningfully outdated.

The instruments genuinely available to an investor with ₹1 crore today include: bank and corporate FDs, listed corporate bonds (NCDs) with monthly coupons, invoice discounting on large corporate and PSU buyers, asset leasing on solar panels and commercial vehicles, Securitised Debt Instruments (pools of auto loans, gold loans), REITs and InvITs (real asset income with daily liquidity), tax-free PSU bonds, Sovereign Gold Bonds, and at exactly the ₹1 crore threshold Category I, II, and III Alternative Investment Funds.

The unifying principle across all of these: each delivers a defined or predictable return stream not equity-style capital appreciation dependent on market sentiment. That is what makes them "fixed income" in the broad sense used in this article, even though several (invoice discounting, asset leasing, SDIs) sit in the "alternative investments" category rather than traditional debt.

The Default Portfolio: What Most ₹1 Crore Sits In

| Allocation | Amount | Gross Rate | Post-Tax Income (30% bracket) |

|---|---|---|---|

| Bank FDs (1-2 year, various PSU/private banks) | ₹85 Lakhs (85%) | 6.6%-6.85% | ₹3.91-4.06 Lakhs |

| Savings account / liquid fund | ₹15 Lakhs (15%) | 3.5%-6.5% | ₹0.46-0.68 Lakhs |

Total default portfolio post-tax income: approximately ₹4.4-4.7 lakhs annually a blended post-tax yield of roughly 4.4-4.7%, barely at or below the 4.5% inflation rate. This is the starting point most investors with ₹1 crore are working from, often without having made a deliberate choice it is simply where money accumulates by default through salary deposits and maturing FDs rolled into new FDs.

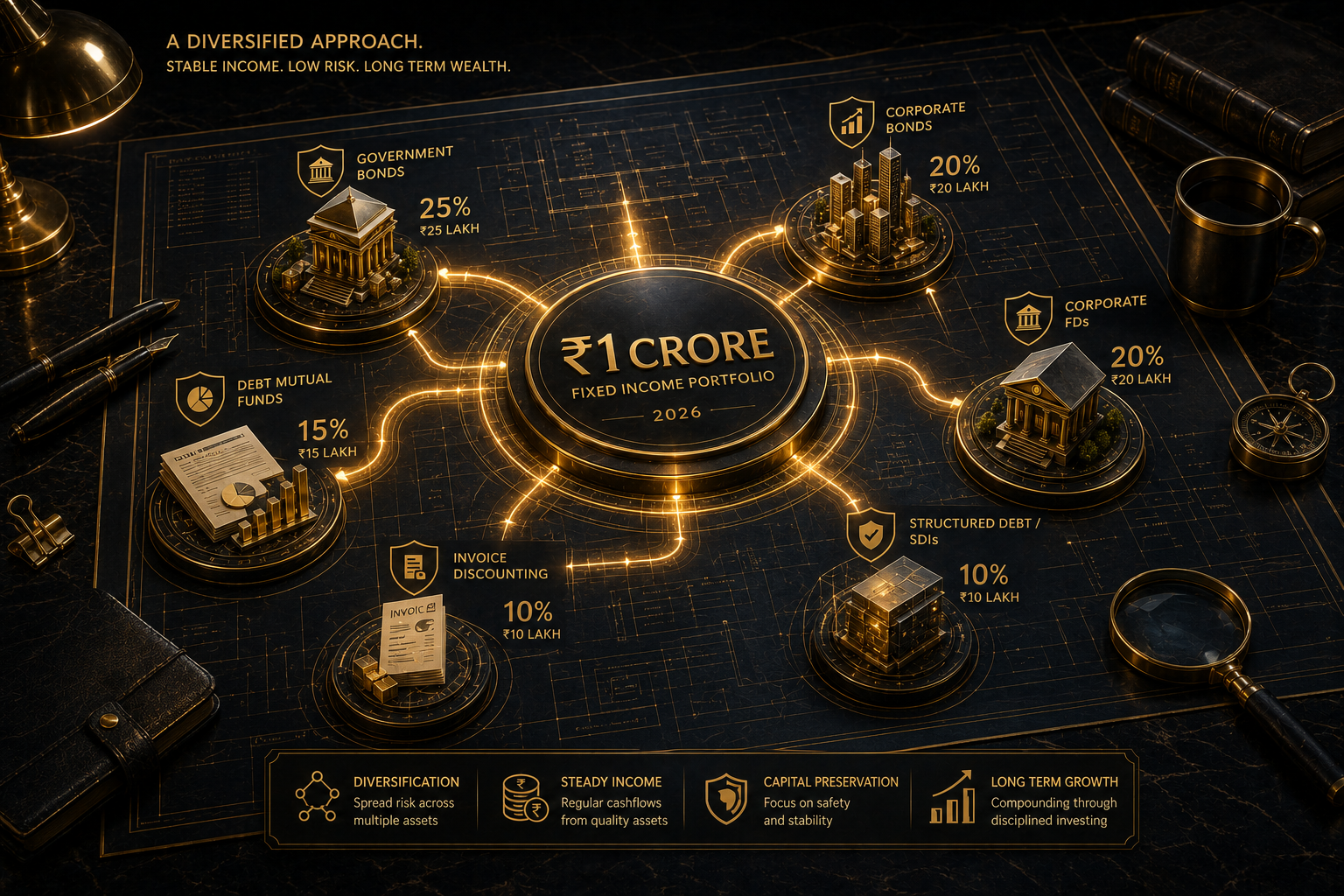

The Allocation Framework: Seven Buckets

| Bucket | Allocation % | Amount | Function | Gross Yield Range |

|---|---|---|---|---|

| 1. Liquidity Buffer | 10% | ₹10 Lakhs | Emergency fund, DICGC coverage, reinvestment reserve | 4.5%-6.85% |

| 2. Invoice Discounting | 25% | ₹25 Lakhs | Liquid alternative yield, 30-90 day recycling, near-monthly income | 11%-13% |

| 3. AA Corporate Bonds | 20% | ₹20 Lakhs | Fixed income core, monthly coupon, listed liquidity | 9.5%-10.5% |

| 4. Asset Leasing | 15% | ₹15 Lakhs | Long-tenure monthly income, tangible asset backing | 11%-15% |

| 5. Securitised Debt Instruments | 10% | ₹10 Lakhs | Pool-diversified fixed income, above-bond yield | 10%-12% |

| 6. REITs / InvITs | 10% | ₹10 Lakhs | Real asset income, daily exchange liquidity | 8%-10% |

| 7. Tax-Free Bonds / SGBs | 10% | ₹10 Lakhs | Tax-efficient income, inflation hedge | 5.5%-8%+ (varies by instrument) |

Bucket 1: Liquidity Buffer (10% ₹10 Lakhs)

What goes here: Bank FDs split across 2 banks (₹5 lakhs each, to maximise DICGC coverage at ₹5 lakhs per depositor per bank) and/or a liquid mutual fund for the portion needing same-day access.

Why 10%: This is the layer that exists for a reason other than yield it is your insurance against needing capital faster than any other bucket can provide it, and it is the reservoir from which you redeploy capital as invoice discounting and other shorter-tenure instruments mature and need reinvestment.

Post-tax income at 30% bracket: ₹10L × ~6.7% gross × 69% (after tax) ≈ ₹46,200/year

For the detailed argument on why liquidity matters disproportionately in HNI portfolios, read: The Importance of Liquidity in HNI Fixed Income Portfolios

Bucket 2: Invoice Discounting (25% ₹25 Lakhs)

What goes here: 15-20 invoice discounting deals across Tier 1-2 buyers (large listed corporates and PSUs), laddered across 30, 60, and 90-day tenures to create near-continuous reinvestment cycles.

Why 25% the largest single allocation: Invoice discounting on strong buyers delivers the best risk-adjusted post-tax yield available at this corpus size. At 12% gross, post-tax at 30% bracket is 8.26% a full 3.5+ percentage points above the liquidity buffer. The 30-90 day tenure means this ₹25 lakhs is constantly recycling providing the portfolio's most active income stream.

Post-tax income at 30% bracket: ₹25L × 12% gross × 69% (after tax) ≈ ₹2,07,000/year

Effective monthly income (laddered): approximately ₹15,000-17,500/month post-tax

For the detailed mechanics of how this income arrives and compounds, read: Invoice Discounting Returns: What 10-12% Yields Actually Look Like

Bucket 3: AA Corporate Bonds (20% ₹20 Lakhs)

What goes here: A bond ladder of AA and A-rated NCDs with monthly coupon options, spread across 6-8 issuers in different sectors (NBFCs, infrastructure, manufacturing) and tenures of 2, 3, and 5 years.

Why 20%: Corporate bonds provide what invoice discounting does not multi-year locked-in yields with monthly coupon predictability and exchange-listed liquidity (you can sell before maturity if genuinely needed, subject to secondary market pricing). At 10% average yield, this bucket anchors the "core fixed income" function of the portfolio.

Post-tax income at 30% bracket: ₹20L × 10% gross × 68.8% (after tax) ≈ ₹1,37,600/year

Diversification discipline: No single issuer should represent more than 10-15% of this bucket meaning no more than ₹2-3 lakhs in any one NCD issuer.

Bucket 4: Asset Leasing (15% ₹15 Lakhs)

What goes here: 3-5 asset leasing deals across solar panel leasing (10-14% yield, 36-60 month tenure, lowest depreciation risk) and commercial vehicle leasing (12-16% yield, 24-48 month tenure, active secondary market for residual value).

Why 15%: Asset leasing provides genuine monthly income (principal + return included in each payment) over a 2-5 year horizon with physical asset backing a structurally different risk profile from unsecured bonds. It is the "set and forget" layer that does not require the active reinvestment management invoice discounting demands.

Post-tax income at 30% bracket: ₹15L × 13% gross (blended) × 69% (after tax) ≈ ₹1,34,550/year

For the complete asset leasing guide including residual value considerations, read: Asset Leasing Investment in India: How It Works & What Returns to Expect

Bucket 5: Securitised Debt Instruments (10% ₹10 Lakhs)

What goes here: AA-rated SDIs backed by pools of auto loans or gold loans from established NBFCs (Shriram Finance, Sundaram Finance, Muthoot), offering built-in diversification across thousands of underlying borrowers.

Why 10%: SDIs offer 50-150 basis points above equivalently-rated single-issuer bonds, with the structural protections of overcollateralisation and excess interest spread absorbing defaults before investors are affected. This bucket adds yield enhancement with a genuinely different risk structure (pool-based, not single-issuer) than Bucket 3.

Post-tax income at 30% bracket: ₹10L × 11% gross × 68.8% (after tax) ≈ ₹75,680/year

Bucket 6: REITs and InvITs (10% ₹10 Lakhs)

What goes here: A mix of listed REITs (Embassy REIT, Mindspace REIT, Brookfield India REIT) and InvITs (PowerGrid InvIT, IRB InvIT), purchased on NSE/BSE.

Why 10%: This is the only bucket in the entire portfolio offering daily exchange liquidity at above-FD yields. With RBI rate cuts improving REIT NAVs and India's commercial office market tightening, 2026 is a constructive entry point. This bucket functions as a secondary liquidity layer beyond Bucket 1 if the liquidity buffer is depleted, REIT/InvIT units can be sold same-day, subject to market price.

Post-tax income at 30% bracket: ₹10L × 9% distribution × ~85% (blended tax treatment) ≈ ₹76,500/year

Bucket 7: Tax-Free Bonds / SGBs (10% ₹10 Lakhs)

What goes here: A split between secondary-market tax-free PSU bonds (NHAI, PFC, IRFC currently yielding ~5.5% YTM, fully tax-free) and Sovereign Gold Bonds held to maturity (CGT-exempt under Section 10(47), with gold price exposure as an inflation/geopolitical hedge).

Why 10%: This bucket serves the tax-efficiency and inflation-hedge functions that the other six buckets do not. At higher tax brackets (above ₹50 lakhs income), the 5.5% tax-free yield on PSU bonds is equivalent to a 7.99%+ taxable yield competitive with AA corporate bonds without adding credit risk.

Post-tax income at 30% bracket: ₹10L × ~6.5% blended (assuming 50/50 split with modest SGB appreciation) ≈ ₹65,000/year

The Complete Portfolio: Income, Liquidity, and Risk Summary

| Bucket | Amount | Annual Post-Tax Income | Liquidity | Primary Risk Type |

|---|---|---|---|---|

| 1. Liquidity Buffer | ₹10L | ₹46,200 | Immediate (with FD penalty) | Minimal (DICGC-covered) |

| 2. Invoice Discounting | ₹25L | ₹2,07,000 | 30-90 day lock per deal | Buyer credit risk (Tier 1-2, low) |

| 3. AA Corporate Bonds | ₹20L | ₹1,37,600 | Listed (secondary market) | Issuer credit risk (AA, low) |

| 4. Asset Leasing | ₹15L | ₹1,34,550 | Very low (24-60 month lock) | Lessee + asset/residual risk |

| 5. SDIs | ₹10L | ₹75,680 | Low (hold to maturity) | Pool credit risk (diversified) |

| 6. REITs/InvITs | ₹10L | ₹76,500 | Daily (exchange-listed) | Market price volatility |

| 7. Tax-Free Bonds/SGBs | ₹10L | ₹65,000 | Moderate (secondary market) | Minimal (AAA PSU / sovereign) |

Total annual post-tax income: approximately ₹7,42,530 against the default portfolio's ₹4.4-4.7 lakhs. The difference is approximately ₹2.7-3.3 lakhs per year, or roughly ₹27-33 lakhs over 10 years before accounting for the compounding effect of reinvesting this additional income.

Blended portfolio post-tax yield: approximately 7.4% compared to 4.4-4.7% for the default portfolio.

Above ₹1 Crore: When AIFs Enter the Picture

₹1 crore is precisely SEBI's minimum investment threshold for Category I, II, and III Alternative Investment Funds. For an investor at exactly ₹1 crore, committing the entire corpus to a single AIF would represent dangerous concentration which is why the constructed portfolio above does not include an AIF allocation.

The practical guidance: AIFs become a reasonable portfolio component once total fixed income corpus reaches ₹2-3 crore or more at which point a ₹1 crore AIF commitment (typically Category II private credit, offering 12-18% gross / 10-14% net of fees) represents 30-50% of the total corpus rather than 100% of it. At ₹1 crore total corpus, the seven-bucket structure above provides genuine diversification; introducing an AIF would mean either under-allocating to it (defeating its purpose as a meaningful position) or over-concentrating.

For investors at ₹2 crore+ considering this step, read: Private Credit Funds in India: Category II AIF Guide for HNIs

Rebalancing: How Often and What Triggers It

Quarterly review, not quarterly rebalancing. The portfolio's allocation percentages should be reviewed every quarter, but wholesale rebalancing should be reserved for specific triggers:

Trigger 1 Invoice discounting maturities. Bucket 2 recycles every 30-90 days by design. Each maturity is a reinvestment decision, not a rebalancing event redeploy into new deals maintaining the buyer-tier and tenure discipline.

Trigger 2 Significant rate environment shifts. If RBI moves rates meaningfully (50bps+), the relative attractiveness of locking in long-tenure bonds (Bucket 3) versus shorter alternatives shifts. A falling-rate environment argues for locking in current bond yields sooner; a rising-rate environment argues for shorter durations.

Trigger 3 Credit events. A rating downgrade on a held NCD issuer, a delayed payment pattern emerging on an invoice discounting buyer, or a lessee default in the asset leasing bucket these warrant immediate review of that specific position, not the whole portfolio.

Trigger 4 Annual tax planning. Once a year, review whether the tax-free bonds/SGB allocation (Bucket 7) should be adjusted based on the investor's actual income bracket for that financial year particularly relevant if income has crossed a surcharge threshold (₹50L, ₹1Cr, ₹2Cr) during the year.

Ultra's Position: The Portfolio We Would Actually Build

Applying the audit principle Ultra's specific view, not a generic "diversify and consult an advisor" conclusion:

For an HNI with exactly ₹1 crore in fixed income surplus in 2026, the seven-bucket allocation above with invoice discounting at 25% as the largest single position is the structure we would recommend, and it is structurally similar to what we observe among Ultra's most engaged HNI investors.

The reasoning for invoice discounting's 25% weight is specific: at this corpus size, ₹25 lakhs is large enough to spread across 15-20 deals for genuine buyer diversification, while the 30-90 day recycling means this capital is never "stuck" it is the most actively working money in the portfolio. The post-tax income from this single bucket (₹2.07L) exceeds the combined income from the liquidity buffer and tax-free bonds buckets combined, on less capital than either of those two buckets combined with Bucket 6.

Where we would push back on conventional advice: Many traditional wealth management approaches for ₹1 crore portfolios over-allocate to bank FDs (40%+) on the rationale of "safety first." Our view: the safety differential between a Tier 1 PSU buyer invoice discounting deal and a bank FD above the ₹5 lakh DICGC threshold is narrower than commonly assumed both involve taking credit risk on a large institution, just a different one. The yield differential (12% vs 6.85%), however, is not narrow. A 10% allocation to the liquidity buffer (Bucket 1) is sufficient for genuine emergency needs; capital beyond that should be working at the yields Buckets 2-5 offer.

What we would not recommend: Concentrating more than 25-30% in any single bucket, regardless of how attractive its yield including invoice discounting itself. The seven-bucket structure exists specifically to ensure that a credit event, liquidity need, or rate shift in any one bucket does not disproportionately affect the portfolio's overall income.

Start building the invoice discounting and asset leasing components of this portfolio at www.getultra.club curated deals on Tier 1-2 buyers with portfolio XIRR tracking built in.

FAQs

Q1. How much post-tax income can ₹1 crore generate in fixed income in India in 2026?

A default bank-FD-heavy portfolio generates approximately ₹4.4-4.7 lakhs post-tax annually (30% tax bracket) a blended yield of roughly 4.4-4.7%. A diversified portfolio across invoice discounting, corporate bonds, asset leasing, SDIs, REITs, and tax-free bonds can generate approximately ₹7.4-8.5 lakhs post-tax annually a blended yield of roughly 7.4-8.5%. The difference is approximately ₹2.7-3.8 lakhs per year, or ₹27-38 lakhs over 10 years.

Q2. What is the best allocation for a ₹1 crore fixed income portfolio?

A balanced structure for 2026: 10% liquidity buffer (bank FDs/liquid funds), 25% invoice discounting (Tier 1-2 buyers, 30-90 day tenures), 20% AA corporate bonds (monthly coupon, 2-5 year ladder), 15% asset leasing (solar/commercial vehicles, 24-60 month tenure), 10% Securitised Debt Instruments (AA-rated pools), 10% REITs/InvITs (daily liquidity), and 10% tax-free bonds/SGBs (tax efficiency and inflation hedge).

Q3. Should ₹1 crore go into an AIF?

₹1 crore is SEBI's minimum for Category I, II, and III AIFs, but committing the entire corpus to one AIF creates dangerous concentration and illiquidity (3-7 year lock-ins). AIFs become appropriate once total fixed income corpus reaches ₹2-3 crore or more, at which point a ₹1 crore AIF commitment represents a reasonable 30-50% of the total rather than 100%.

Q4. How much should be in bank FDs in a ₹1 crore portfolio?

Approximately 10% (₹10 lakhs), split across 2 banks to maximise DICGC coverage (₹5 lakhs per depositor per bank). This serves as the emergency fund and reinvestment reserve not as a primary income-generating allocation. At 30%+ tax brackets, bank FD post-tax returns are at or below inflation, making larger FD allocations a drag on overall portfolio yield.

Q5. How often should a ₹1 crore fixed income portfolio be rebalanced?

Review quarterly, but rebalance based on specific triggers rather than a fixed schedule: invoice discounting maturities (every 30-90 days, requiring reinvestment decisions), significant RBI rate moves (50bps+), credit events affecting specific holdings (rating downgrades, payment delays), and annual tax planning reviews particularly if income crosses a surcharge threshold during the year.

Q6. What is the difference between this portfolio and a debt mutual fund portfolio?

Debt mutual funds pool investor capital into a fund structure with NAV-based returns and fund-level taxation. The seven-bucket portfolio in this article uses direct instruments individual bonds, direct invoice discounting deals, direct asset leasing positions giving the investor direct ownership, defined yields known in advance, and no fund management fees. The trade-off is more active involvement in selecting and monitoring individual positions versus a single fund subscription.

Disclaimer

This article is for informational and educational purposes only and does not constitute investment advice. Returns are indicative based on current 2026 market conditions and may change. All investments carry risk including loss of principal. Allocation percentages are illustrative and should be adjusted based on individual risk tolerance, liquidity needs, and tax circumstances. Please consult a SEBI-registered investment advisor before implementing any portfolio strategy.